Each case must be considered under its facts and circumstances. Although our Recent Victories reflect many of our outright dismissals, it is essential to know that settlement — especially in the context of a frozen bank account — is often the desired outcome. Settlement is certain. The settlement resolves the judgments "on the merits" (forever) versus a dismissal of a technical nature, which could leave the creditor's claim open.

Settlement may be desired even in debt-buyer cases with weak underlying evidence. The fact is that upon enforcement (i.e. bank seizure), you are the judgment debtor with the considerable burden of re-opening the case and requesting that the court excuse your default. Even with good defenses, many clients prefer a good settlement to resolve the matter faster. Speed and certainty are often desired over cost and uncertainty. Judges have considerable discretion as to whether to overturn a judgment.

Facing a frozen bank account because of a judgment by LVNV Funding for $23,917 entered in 2011, we quickly asserted our client's exemptions and struck a quick settlement for roughly 25%. Our client was aware of prior judgment activity involving the same case, which hurts the argument that he was unaware of judgment.

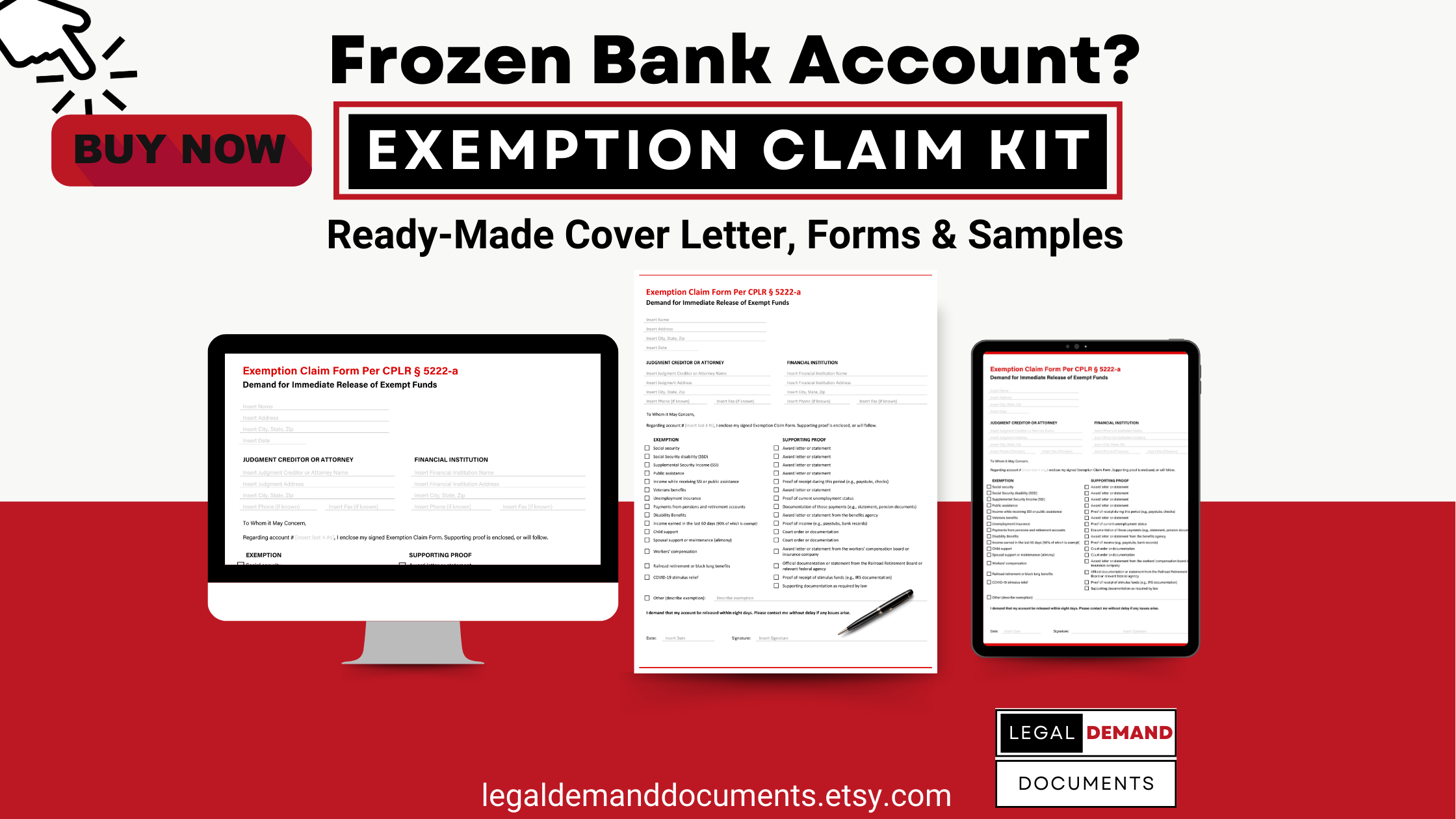

Upon a bank account seizure, I highly suggest contacting counsel to review the exemption sources to see what applies. Asserting these exemptions (including 90% of income earned within the last 60 days) is often critical for stopping a levy.

To avoid searching for lawyers and paying thousands in fees, we've created a set of forms (with instructions) to get a release on your own:

The Interplay of Settlement and Bank Restraints

When facing a frozen bank account due to a creditor's judgment, the primary goal is often to regain access to your funds as swiftly as possible. In such cases, settlement can be a desirable path, mainly when the account contains exempt funds, such as social security, pensions, or wages. Considering the burden of proof, legal costs, and time involved, it’s essential to weigh the benefits of a quick settlement against the potential of fighting the case.

Key Considerations in Settlement Decisions:

Speed and Certainty vs. Legal Battle: Settlement offers a definitive conclusion to the debt issue, bypassing the uncertainties and delays of legal proceedings. In scenarios where exempt funds are frozen, a quick settlement can provide immediate financial relief.

Understanding the Burden of Proof: As the judgment debtor, the responsibility to challenge the judgment or prove exemptions falls on you. This can be a daunting task, requiring substantial legal knowledge and, often, the assistance of counsel.

Evaluating the Settlement Offer: Assess the creditor's offer critically. A settlement for a fraction of the original judgment, as in the LVNV Funding case, can be a financially sound decision, particularly when considering the costs and time of litigation.

Awareness of Prior Judgments: Previous judgment activities can influence your position in negotiating a settlement. Awareness of past judgments and how they impact your case is crucial.

Asserting Exemptions in the Context of Settlement

When exempt funds are involved in a frozen account, promptly asserting these exemptions is vital. It protects a portion of your funds and can strengthen your position in settlement negotiations. For instance, under New York law, up to 90% of income earned in the last 60 days may be exempt, which can be a significant factor in discussions.

![]()

![]()