1) Account Stated is a “cause of action.” What is a cause of action?

A cause of action has two definitions:

- noun. A condition under which one party would be entitled to sue another.

- noun. A set of facts that, if true, entitle an individual or entity to be awarded a remedy by a court of law.

A cause of action is used synonymously with “theory” or “legal theory.” They’re all used to encompass facts that give a party the right to seek a legal remedy against another. In this context, it gives a creditor the right to sue for money owed.

2) What is the definition of Account Stated?

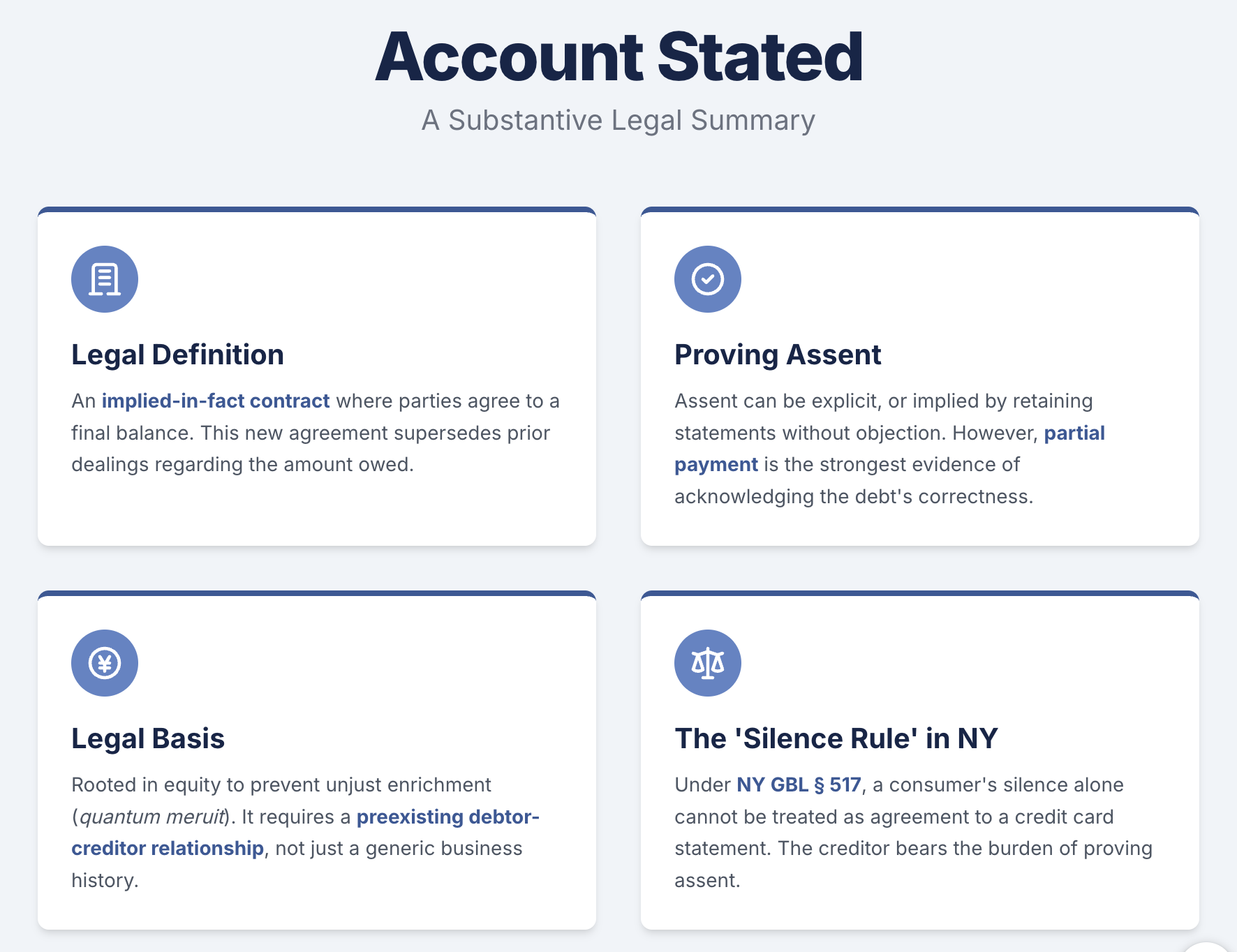

An Account Stated is a manifestation of assent by a debtor and a creditor to a stated sum as an accurate computation of an amount due to the creditor."[1] It’s a promise to pay a pre-existing debt without promising anything new in return (“consideration”).

3) What is “Account Stated” in debt collection?

An account stated is an agreed balance between the parties. It serves as the collector’s legal theory—and the amount of money—to prove your liability for it. In New York, a billing statement can support an account‑stated claim only when the debtor expressly or implicitly assents (e.g., by retaining it without timely objection or by making payments); mere silence is insufficient under General Business Law § 517. Once accepted, the statement becomes a new contract.

4) What are the legal elements of an account stated?

To state a claim for an account stated, a plaintiff must allege:

- An account was presented;

- The account was accepted as correct, and

- The debtor promised to pay the account.[2]

5) Is silence an admission to the statement (amount) of the account?

It can be. Although in some commercial settings silence may evidence assent, New York law forbids credit‑card issuers from treating silence alone as conclusive acceptance of a balance (GBL § 517).[3]

6) Why do collectors use Account Stated in debt-collection cases?

Account stated is used when collectors or debt buyers want to avoid showing how the final amount was computed and to avoid having to prove the terms of the written contract. It is a new contract that supersedes the prior, written contract. However, an account stated must attach to an “original liability” such as an underlying contract. In other words, an account stated relies on a preexisting legal relationship to form the “new” contract.

7) Can an Account Stated result in a default judgment in New York?

Yes. Clerks may issue defaults under CPLR § 3215 for unanswered complaints alleging Account Stated theories—under the following conditions:

1. The affidavit of facts or verified complaint verifies that an accounting was sent to the defendant.

2. The affidavit of facts or verified complaint must affirm that the defendant retained the accounting and that no objection to it has been made.[4]

Here is a City Court Directive, signed by Administrative Judge Fern Fisher-Brandveen in 2001, which permits seeking default judgments for Account Stated causes of action. The Directive rescinded the court’s earlier practice of requiring the waiver of Account-Stated theories if one or more causes of action were presented in the complaint. Since the 2014 statewide rules and the 2022 Consumer Credit Fairness Act, a plaintiff seeking a CPLR 3215 default on a consumer‑credit account‑stated claim must file the mandated original‑creditor affidavit, statute‑of‑limitations affidavit, and additional notices before the clerk may enter judgment.

8) Does the plaintiff need a signed credit card agreement to prove an Account Stated?

No. However, the plaintiff does have to prove a potential right under a preexisting relationship. Conceptually, an Account Stated forms a new, implied contract based on the old contract. It’s a second cause of action for an implied contract.

9) How did an Account-Stated claim become recognized?

Before present-day contract law, Account Stated was created for people and businesses with an open series of accounts for various debit and credit items. The parties convened to “compare books, memories, mutual accounts, and strike a balance.”[5] Such parties included bankers and depositors, customers and grocers, and business partners.

10) Is Account Stated legally based on a preexisting contract?

Not necessarily. Tricky question, though. A preexisting contract, if one was entered into, may form the basis of an Account Stated cause of action. A preexisting contract is one way to establish a pre-existing legal relationship showing indebtedness under Account Stated. An account‑stated claim must be grounded in prior transactions that created a debtor–creditor relationship; a generic ‘business relationship’, standing alone, will not suffice.

11) What is the creditor’s burden of proof for an Account Stated claim?

Like any civil case, it is a preponderance of evidence (greater than 50%).

12) How is Account Stated differently from a breach of contract?

An Account Stated establishes an implied contract, whereas a breach of contract traditionally refers to an expressly written contract. Account Stated is used when no contract exists or when the plaintiff cannot prove the existence of the contract. Account stated is an independent theory that may be pleaded alongside breach of contract; courts dismiss one as duplicative only when both claims seek identical relief on the same facts.. Account Stated, however, does not prove the validity of each charge as would a breach of contract.

13) What is the “statement” for purposes of an account-stated claim?

Bank statements or invoices, generally. The court will honor “credible evidence of actual charges.” Of course, all business records must go through hearsay hurdles in order to be admissible. For ideas on how to attack the admissibility of business records, check out 11 Questions to Raise in a Debt-Buyer Lawsuit: Authenticity of Electronic Reproductions.

14) What is the statute of limitations for an Account Stated claim?

For consumer‑credit actions filed on or after April 7 2022, the statute of limitations is three years (CPLR 214‑i); earlier‑accruing or non‑consumer claims remain subject to the six‑year period in CPLR 213(2). The clock usually starts on the date the account first went into default (e.g., the missed payment), not the last purchase. For non-consumer debt, it's six years in New York. See a full discussion of the Statute of Limitations here.

15) Is Account Stated an express or implied contract between the parties?

Account Stated is an implied contract based on a preexisting relationship between the parties. Repeated use of the card may evidence a course of dealing, but an account‑stated claim still requires proof that the debtor assented to the final balance—typically by paying or by keeping the statements without timely objection. Borrowers would gain windfalls by lenders who simply failed to preserve all contractual evidence.

16) Why do debt collectors allege an Account Stated when their case is really based on a contract (credit-card agreement)?

Account Stated is used when creditors or debt buyers lack access to an admissible contract. It’s an additional legal theory to help creditors get paid without having to produce the contract. It also prevents windfalls for borrowers. It’s rooted in the Latin phrase, Quantum Meruit (“as much as is deserves”)—an equitable principle that prevents unfairness by compensating people who are at a loss.

17) Can debt buyers allege “Account Stated” theories?

In New York, yes. However, the statement of account must also be introduced properly as a business record. That introduction is usually done by affidavit. The affidavit must be based upon personal knowledge and otherwise be credible. An employee of the debt buyer is not qualified to produce an affidavit that authenticates an originating creditor’s account statements.

18) In New York, does silence alone prove the correctness of the creditor’s statement?

No. In fact, a New York statute[6] prohibits these presumptions of silence. Credit card agreements may not require that a credit card account be deemed correct just because a consumer fails to object to it within a specified period of time. Here is the law:

General Business Law § 517 Statements of account

No agreement between the issuer and the holder shall contain any provision that a statement sent by the issuer to the holder shall be deemed correct unless objected to within a specified period of time. Any such provision is against public policy and shall be of no force or effect.

But partial payment is an acknowledgment of the correctness of the account.[7] There is strong evidence of an implied agreement where there is a partial payment coupled with a promise to pay the balance.[8]

An interesting Vermont case holds that silence alone is not enough to demonstrate assent to a final balance. It reasoned that “credit card statements often contain multiple interest rates, interest rates which fluctuate from billing period to billing period, and a myriad of other kinds of fees and penalties.”[9]

That court went on to further hold:

"While the credit cardholder, looking at the statement, can see the amount of the charges that were imposed, he or she is unlikely to know whether the charges are consistent with the writings governing the cardholder's obligations." Target Nat'l Bank/Target VISA at 11. Since credit cardholder member agreements are potentially confusing because of the format and complexity of the language, the average cardholder likely has difficulty understanding them and determining whether the charges and fees comply with the agreement. See Credit Cards, GAO-06-929. Because the Court does not agree that Ms. Cooper's silence was tantamount to assent to the accuracy of the monthly statements, the Court finds that Citibank has not proved an essential element of its account stated claim. The Court denies Citibank's Motion for Summary Judgment on the account stated theory."

Nonetheless, some courts find that silence is enough for implied consent, particularly if a consumer has regularly paid a series of statements.

19) Who has the burden of proof as to your assent to the final balance?

The collector is the one with the burden of proving all elements of its cause of action, so the collector has the burden of showing the consumer’s agreement to pay the charges and thus has the burden of showing that silence upon receiving the statement shows consent.[10]

20) What evidence qualifies as an agreement of the amount due?

Any allegations of fact showing that you retained updated statements without objection. Also, paying the card, especially after a disputed charge, is argued as an acknowledgment of the correctness of the account.

21) How does the collector prove that I retained the statement(s) without objection?

Each case involves a different set of facts, all of which should be considered. With banks and credit card statements, consumers are outgunned and confused as to their rights. I would guess that few objections are effectively made to statement balances. Banks rely heavily on your payments on the card as proof that you’re happy, not objecting, and therefore in acknowledgment of the current balance. Paying a credit card statement, even a disputed credit card statement, may infer the assent element of Account Stated.

But in Citibank (South Dakota) v. Brown-Serolvic,[11] small payments alone do not “create the inference of assent.” Also, a bank’s affidavit must allege that the consumer received, without objection, the bank statement(s) at issue. The point here is that banks need to allege that you received the statements and did not object.

Similarly, in American Express Centurion Bank v. Cutler,[12] the court held that Amex did not allege facts showing that the consumer retained billing statements for an “unreasonable period of time” without objecting to them. Nor did the bank allege that the consumer made partial payments on the billing statements. Again, the point here is that banks need to prove all elements of an account-stated claim if one is relied upon in the case.

At a bare minimum, the collector must prove that the statement was sent to the consumer.[13]

Six more arguments against an Account Stated theory

- The Account Stated is only for the minimum amount owed—not the full balance (crafty).

- Under federal law, the creditor must, when challenged, prove all transactions leading up to the final balance. Credit card holders have the burden of proof to demonstrate the full basis of the cardholder’s liability.[14]

- An Account Stated is not consistent with money sought by the Plaintiff, including finance charges, prejudgment interest, fees, and attorneys’ fees. Stated another way, the plaintiff did not prove its entitlement to, and application of, fluctuating interest rates, charges, and fees with its account statements alone.

- The statements produced do not show a payment, which is the minimum requirement to show assets to the latest account. Actual payment is better proof of acknowledgment of the correctness of the account.

- Debt buyers who buy only contractual claims from the original creditor may not sue for unjust enrichment or an implied contractual theory of Account Stated.

- Account statements showing a zero balance (after charge-off) establish zero liability.

After digging in the blog crates, I noticed that we already reported on the Amex v. Cutler, cited above, for the holding that Amex failed in its burden to prove the retained-without-objection element. In Cutler, a small payment toward the larger balance did not preserve the case, especially in light of previously disputed charges.

Key Insights into 'Account Stated': Silence, Assent, and Burden of Proof

Understanding of Account Stated: 'Account Stated' is a legal concept used in debt collection, representing an implied contract between the debtor and creditor based on a preexisting relationship. It is an agreed balance between the parties that serves as the collector's legal theory to prove liability. It does not necessarily have to be based on a preexisting contract but can be alleged based on a business relationship alone.

Silence and Assent: In some cases, silence can be interpreted as an admission to the statement (amount) of the account. Not objecting to an inaccurate charge or amount within a "reasonable time" can be argued as an admission of the amount due. However, the New York statute prohibits presumptions of silence, and the collector must prove all elements of its cause of action.

Burden of Proof: The burden of proof for an 'Account Stated' claim lies with the collector, who must prove that the statement was sent to the consumer and that the consumer retained the statement without objection. Paying the card, especially after a disputed charge, may infer the assent element of 'Account Stated', but small payments alone do not create the inference of assent.

Quiz to Test Comprehension

What is a 'cause of action' in legal terms?

- A) A legal claim filed in court.

- B) A condition under which one party can sue another.

- C) A finalized court judgment.

What best defines 'Account Stated'?

- A) A written agreement between debtor and creditor.

- B) A manifestation of assent to a stated sum as an accurate debt amount.

- C) A formal dispute of a debt.

In debt collection, what does 'Account Stated' represent?

- A) An agreed balance between debtor and creditor.

- B) A written acknowledgment of debt.

- C) A request for debt forgiveness.

What are the legal elements required for an account-stated claim?

- A) Account presentation, acceptance, and promise to pay.

- B) Debt verification, legal notice, and payment agreement.

- C) Contract signing, debt acknowledgment, and payment plan.

Can silence be considered an admission to the statement of an account?

- A) Always.

- B) Never.

- C) Yes, in certain situations.

Why do collectors use 'Account Stated' in debt-collection cases?

- A) To avoid showing how the final amount was computed.

- B) To simplify the legal process.

- C) To increase the debt amount.

Can an 'Account Stated' result in a default judgment in New York?

- A) Yes, under certain conditions.

- B) No, never.

- C) Only if the debtor agrees.

Is a signed credit card agreement necessary to prove an 'Account Stated'?

- A) Yes, always.

- B) No, but a preexisting relationship must be proven.

- C) Only in specific cases.

How did an 'Account-Stated' claim originate?

- A) Modern contract law.

- B) Ancient legal practices.

- C) For businesses with open accounts to strike a balance.

Is 'Account Stated' always based on a preexisting contract?

- A) Yes, it's a requirement.

- B) No, but it's often used.

- C) Not necessarily, a business relationship may suffice.

Answer Key:

- B) A condition under which one party can sue another.

- B) A manifestation of assent to a stated sum as an accurate debt amount.

- A) An agreed balance between debtor and creditor.

- A) Account presentation, acceptance, and promise to pay.

- C) Yes, in certain situations.

- A) To avoid showing how the final amount was computed.

- A) Yes, under certain conditions.

- B) No, but a preexisting relationship must be proven.

- C) For businesses with open accounts to strike a balance.

- C) Not necessarily, a business relationship may suffice.

[1] Restatement (Second) of Contracts, Account Stated § 282.

[2] § 4:7. Account stated, 28 N.Y. Prac., Contract Law § 4:7

[3] National Westminster Bank USA v. Seidler, 1984-6547 (Dist. Ct. Nassau Cnty. 1984).

[4] 0See Directive and Procedures 158, Entry of Judgment - Account Stated, Hon. Fern Fisher-Brandveen, Administrative Judge of the Civil Court of the City of New York, July 27, 2001.

[5] Corbin on Contracts, § 1303 at 234.

[6] N.Y. Gen. Bus. Law § 517.

[7] Shea & Gould v. Burr, 194 A.D.2d 369, 598 N.Y.S.2d 261 (1st Dep't 1993);

[8] Boulanger, Hicks, Stein & Churchill, P.C. v. Jacobs, 235 A.D.2d 353, 653 N.Y.S.2d 11 (1st Dep't 1997).

[9] Citibank v. Cooper, 305-10-08, Superior Court, Calendonia County (2009). See U.S. Gov't Accountability Office, Credit Cards Increased Complexity 3 in Rates andFees Heighten Need/or More Effective Disclosures to Consumers, GAO-06-929 (2006). (silence was not tantamount to assent to the accuracy of the monthly statements).

[10] Citibank v. Goldberg, 901 N.Y.S.2d 898 (N.Y. App. Term 2009).

[11] Supreme Court, Appellate Division, Second Department, New York. 97 A.D.3d 522948 N.Y.S.2d 331 (July 5, 2012).

[12] Am. Exp. Centurion Bank v. Cutler, 81 AD3d 761 (2d Dept 2011).

[13] Morrison, Cohen, Singer & Weinstein, L.L.P. v. Brophy, 798 N.Y.S.2d 379 (N.Y. App. Div. 2005).

[14] Carmody-Wait 2d § 36:174