1) What is the statute of limitations?

The statute of limitations is the time period in which a plaintiff has the legal right to sue. It starts from the date of your missed minimum payment. If a collector sues within that time, the statute of limitations STOPS. However, collectors sometimes still sue outside of the statute of limitations, and it’s your job to raise the defense.

In New York, the three primary statutes of limitations in consumer debt-collection cases:

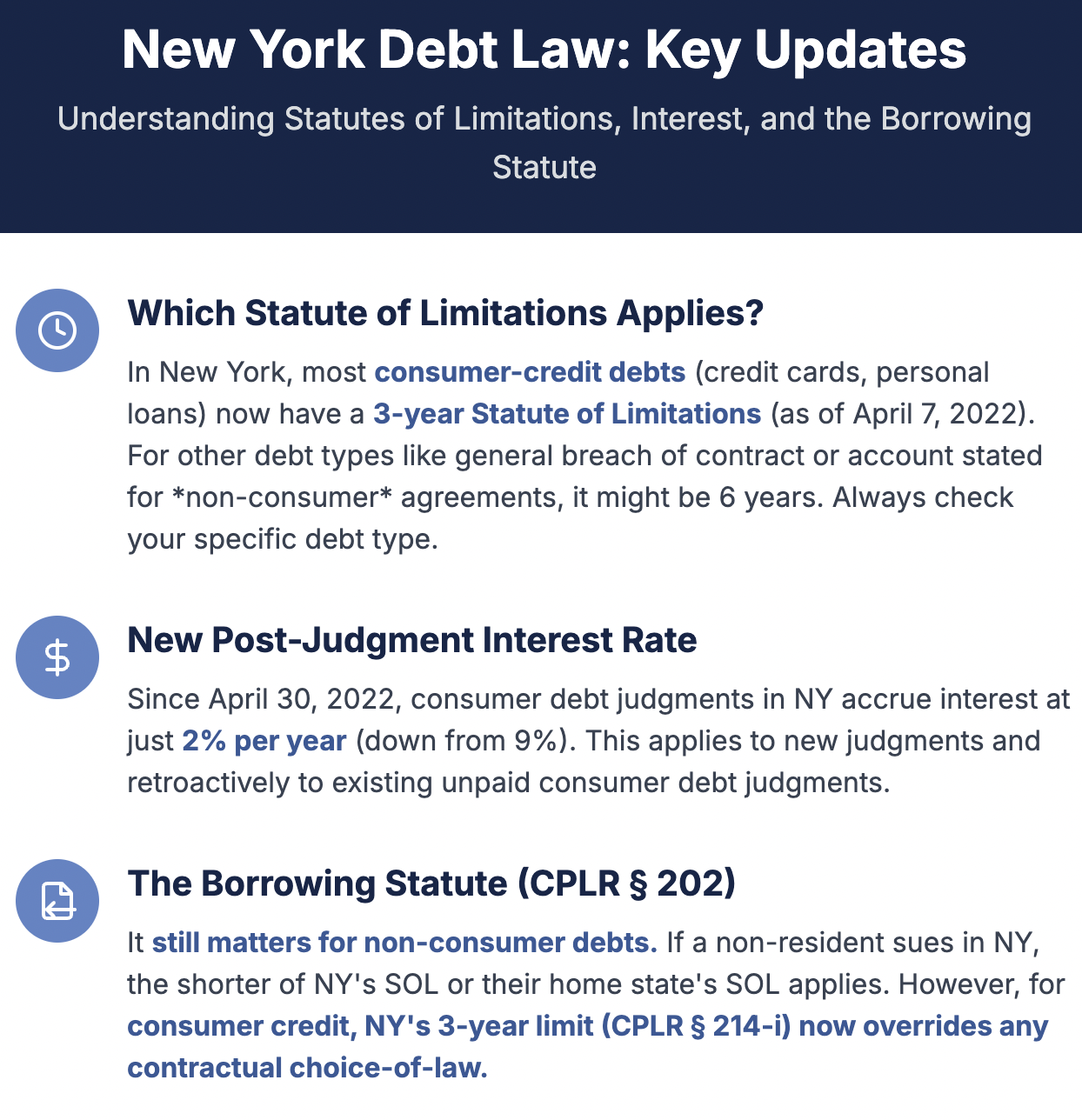

- Breach of Contract: 3 years. It begins to run when you miss a minimum payment. Effective April 7, 2022: The statute of limitations for consumer-credit transactions has been reduced to 3 years per CPLR § 214-i. For our recent blog about this shortened statute of limitations per the Consumer Credit Fairness Act, see 5 Powerful Lawsuit Defenses for New York Debtors in 2022.

- Account Stated: 3 years. It begins to run from your last purchase or payment. Non-consumer agreements would take six years.

- Single purchase of goods (Account Stated): 4 years. It begins to run from your last purchase or payment. UCC § 2-725. This law applies to sales of goods purchased on store credit, like furniture stores and electronic stores.

- Medical Debt: 3 years. It begins to run from the date of treatment. CPLR § 213-d was added April 3 2020 and applies only to hospitals and licensed providers, not to third-party medical-credit cards.

In New York, the law is contained in CPLR § 213.[1] For the statute of limitations in all states, see this chart if and when a collector secures a judgment, a new (often different) time limitation to enforce it applies.

2) What is the purpose of the statute of limitations?

It prevents courts from hearing stale, unreliable evidence. It encourages prompt action and prevents unfair prejudice.

3) What can my credit report tell me about the statute of limitations?

You can confirm your default date using your credit report. The default date (30 days after your last payment) triggers the statute of limitations. This answer can change depending on your state and debt type. The “30,” “60,” or “90” represents the number of days the account is in default.

****Note: Judgments (especially old ones) will not appear on your credit reports. But legally, judgments acquire a new time limitation to be enforced. In New York, judgments are enforceable for 20 years upon entry. The judgment lien on real property lasts only 10 years unless renewed under CPLR § 5014.Consumers often assume that since they don’t see an old debt, an old judgment, or their credit report, the debts or judgments are not valid. Unfortunately, that is a bad assumption. We fight some judgments that are sometimes over 20 years old.

![]()

4) How long do debts stay on my credit report?

Late payments can stay on your report for seven years from the original delinquency. Collection accounts can remain on your credit report for seven years and 180 days from the day of the original delinquency. Worth noting is that negative accounts remain present for 7 years while positive accounts can remain present indefinitely even after closed or paid in full. Win for the consumer!

5) What date triggers the statute of limitations for credit card debt?

The date you defaulted for legal purposes. While a “default” is spelled out in your credit agreement, defaults and the statute of limitations are widely known as follows.

In New York:

***Update: Effective April 7, 2022: The statute of limitations for consumer-credit transactions has been reduced to 3 years per CPLR § 214-i.

- Breach of Contract: 3 years. It begins to run when you miss a minimum payment.

- Account Stated: 3 years. It begins to run from your last purchase or payment.

- Single purchase of goods (Account Stated): 4 years from last purchase or payment. Uniform Commercial Code § UCC § 2-725. This law applies to sales of goods purchased on store credit, like furniture stores and electronic stores.

If you need help, complete this intake form.

6) Do civil judgments appear on my credit report?

No, not since July 1, 2017. This date is when Experian, Equifax, and TransUnion decided to exclude almost all civil judgments and up to 50% of tax liens from credit reports. Now, all tax liens were removed by April 16, 2018 (not just “up to 50 %”). This measure was designed to prevent the mixing of credit files. Since judgments (and tax liens) do not include dates of birth and social security numbers, they were too easily attached to the wrong person. A CFPB final rule (Jan 7 2025) will strip all medical bills from credit reports; industry suit filed Jan 8 2025.

Here’s more detail about this legal development in a treatise written by my favorite consumer lawyers—the National Consumer Law Center!

But keep in mind, judgments and tax liens are still public record, and still impact your ability to qualify for credit or loans.

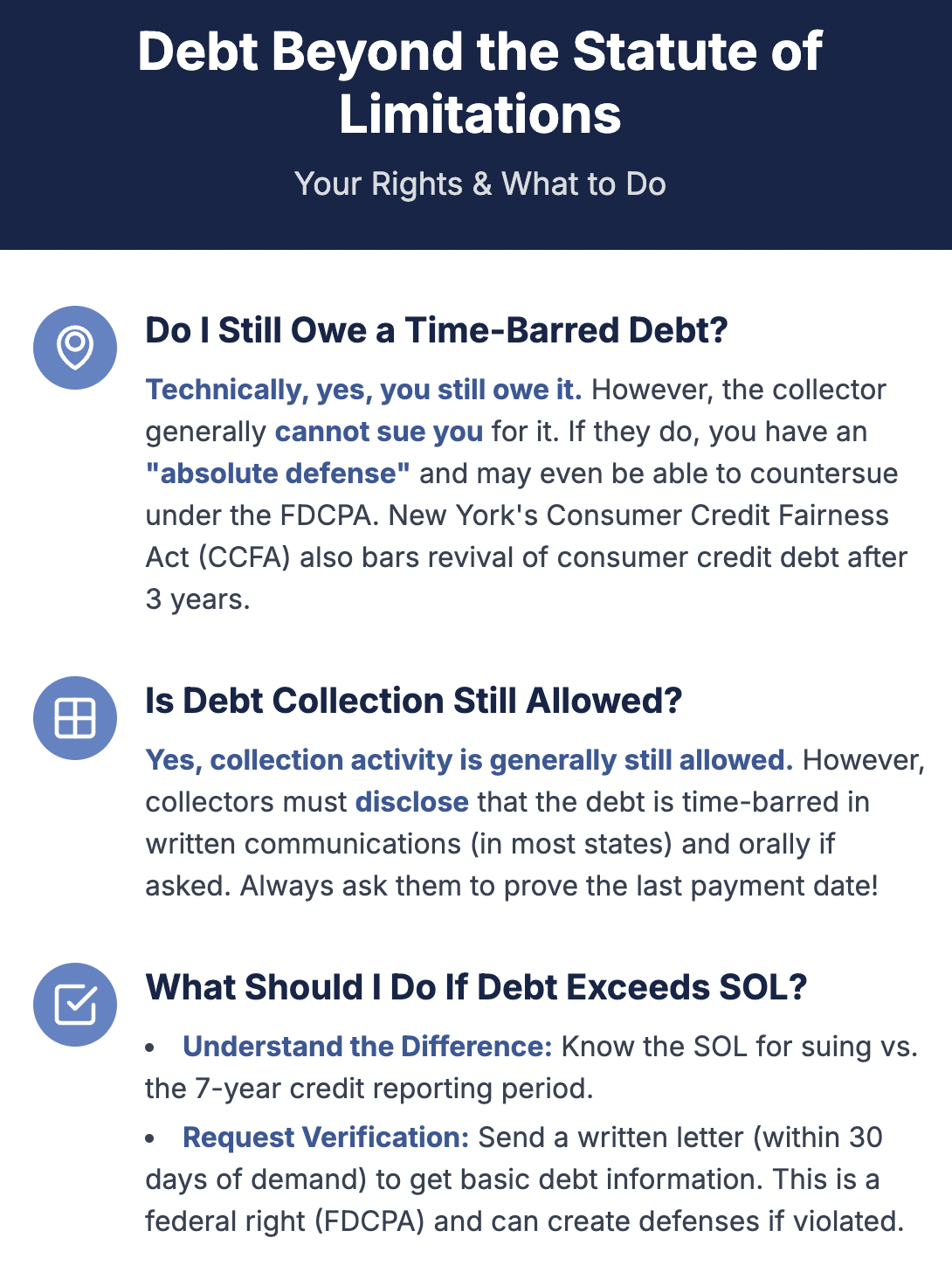

7) Do I still owe a debt past the statute of limitations?

Yes, you technically still owe it. But the collector just can’t sue you for it. Let me modify that. A collector may still sue you, but you now have an “absolute defense” and can countersue for violating the Fair Debt Collection Practices Act. But generally, collection activity is still allowed with certain disclaimers. Whether or not you want to pay it after the statute of limitations is a personal decision. Some feel a moral compulsion to pay. Others do not. Consumer Credit Fairness Act (CCFA) expressly bars revival after the three-year period..

8) Is debt collection still allowed after the statute of limitations?

Yes. However, collectors must disclose this fact in written communications (in most states) and affirm it orally if asked about it. Always ask (orally and in writing) that the collector prove the last payment date.

For practical advice about responding to collection attempts beyond the statute of limitations, see How long a debt collector can pursue old debt? The publisher of that article, Bankrate, Inc., approached our firm to ensure that our clients receive helpful consumer finance tools.

9) What should I do if a debt exceeds the statute of limitations?

First, know the difference between the statute of limitations to sue and the time allowed to report on credit (seven years). Debts that are stale for credit reporting may not be for legal action, and vice versa.

Secondly, request “verification” (a/k/a “validation”) of the debt. This means that you send a written letter (within 30 days of demand) to obtain basic information about the law. The collector is required to provide verification before seeking collection further. If it fails to do so, it violates federal law (FDCPA), forming the basis of possible statutory damages. Unfortunately, debts get bounced between different collection agencies after consumers demand verification. This may force you to send multiple verification demands. The law is conflicting as to whether or not actual notice of a consumer’s dispute is imputed from one collector to another.

Here are well-tailored dispute letters (in Word format) provided by the Consumer Financial Protection Bureau.

10) What Happens If I Pay a Time-Barred Debt?

Legal Statute-of-Limitations (“Legal Clock”)

New York’s Consumer Credit Fairness Act (CPLR § 214‑i), effective April 7, 2022, ensures that once three years have passed since the default, **any subsequent payment or acknowledgment—written or oral—**cannot revive or extend that limitations period.

Credit-Reporting Timeline (“Credit Clock”)

Under federal law (the Fair Credit Reporting Act), the negative information stays on your report for seven years plus 180 days from the original delinquency date—regardless of any later payment Changing payment status doesn’t reset this clock.

11) Is the New York statute of limitations extended due to the Covid-19 (Coronavirus) pandemic?

Through Executive Order No. 202.8,[2] which was extended seven times through follow-up Executive Orders, Governor Cuomo “tolled” all limitations’ periods from March 20, 2020, to November 3, 2020. Although there is some debate as to whether this extension was a “toll” (adds corresponding time to the deadline) versus a “suspension” (extends the deadline date only), treat it like a suspension to err on the side of caution. In 2025, Courts now agree the pandemic orders tolled (paused) SOLs from Mar 20, 2020–Nov 3, 2020; the time left on the clock resumes afterward.

12) How do I raise the statute of limitations defense if I’m sued?

In response to a lawsuit (summons and complaint), you’d raise the statute of limitations in your answer as an affirmative defense, as grounds for a motion to dismiss, or through a summary judgment motion before trial. Push on this defense hard for any credit card governed by a three-year statute of limitations (Chase, BofA, Discover, or Barclays).

13) How do I know which statute of limitations applies?

Check the chart for your state and debt type. In New York, six years is the statute of limitations for breach of contract and account stated theories (the two main legal theories). As of 2022, all consumer-credit causes of action (breach, account stated, unjust enrichment, etc.) are now 3 years.

14) What is the post-judgment interest rate on a consumer-debt money judgment in New York, and how is it applied?

Under the Fair Consumer Judgment Interest Act (L. 2021, ch 751) amending CPLR § 5004, any judgment “arising out of a consumer debt” against a natural person now accrues interest at 2 % per year instead of 9 %. The change took effect on April 30 2022 and (i) governs all consumer-debt judgments entered on or after that date, and (ii) retroactively lowers the rate to 2 % on the unpaid balance of consumer-debt judgments that were already on the books but still outstanding as of April 30 2022.

15) Does the Borrowing Statute Still Matter?

Yes—but only outside the consumer-credit context. CPLR § 202 says a non-resident plaintiff suing in New York must satisfy the shorter of (i) New York’s limitations period or (ii) the limitations period where the claim “accrued” (usually the plaintiff’s home state for purely economic losses).

Before 2022: Some issuers—Chase, Bank of America, Discover, Barclays—invoked Delaware law (three-year limit), while others such as Citibank and Wells Fargo relied on South Dakota’s six-year period.

Now: CPLR § 214-i overrides any contractual choice-of-law clause for New York suits. Whether the account agreement points to Delaware, South Dakota, or Mars, the court must dismiss a consumer-credit case filed more than three years after default.

The “borrowing statute” CPLR § 202:

An action based upon a cause of action accruing without the state cannot be commenced after the expiration of the time limited by the laws of either the state or the place without the state where the cause of action accrued, except that where the cause of action accrued in favor of a resident of the state the time limited by the laws of the state shall apply. CPLR § 202

Key Points for Readers

Uniform Three-Year Limit – All consumer-credit suits (credit cards, personal loans, retail-installment contracts) must now be filed within three years.

No Revival – Partial payments or promises after the three-year mark do not restart the SOL.

Borrowing Statute Lives On – For non-consumer claims—commercial loans, services contracts, etc.—CPLR § 202 can shorten the deadline if the cause of action arose in a state with a tighter SOL than New York’s

Lower Post-Judgment Interest – Even when a timely suit succeeds, post-judgment interest on consumer debts is capped at 2 % (since April 30 2022).

16) Will payment of the debt expunge the negative mark from my credit (“pay for delete”)?

16) Will payment of the debt expunge the negative mark from my credit (“pay for delete”)?

No, not usually. Although some debt buyers agree to delete collection accounts as part of settlements, trends in credit scoring models show that paid collection accounts are becoming increasingly irrelevant.

Also, original creditors like banks frown on such “deals” since they violate the accuracy mandates of the Fair Credit Reporting Act. In litigation, the plaintiff’s lawyers (in my experience) never agree to pay-for-deletions in lawsuits brought by original creditors. As an alternative, you can dispute reporting errors and stale marks, request verification under the FDCPA, or wait for the negative mark to fall off.

17) Ten things people don't know about the Statute of Limitations in New York

Varied Time Frames: Depending on the type of claim, the statute of limitations can range from one year (e.g., for defamation) to twenty years (e.g., for a money judgment).

Tolling: Under certain circumstances, the clock can be "paused" or "tolled." For instance, if the victim is a minor, the clock may not start running until they reach the age of majority.

Discovery Rule: For some claims, the clock doesn't start when the injury occurs but when the injury is or should have been discovered. This is particularly relevant in medical malpractice cases.

Intentional Wrongdoing: For intentional torts like assault, battery, or false imprisonment, the statute of limitations is typically one year from the date of the event.

Medical Malpractice: The general rule is 2.5 years from the date of the malpractice or from the end of continuous treatment rendered by the party or entity you intend to sue.

Wrongful Death: A claim must be brought within two years of the date of death.

Contracts: For a breach of a written contract, the limitation period is six years from the breach, not from when the contract was signed. But for consumer credit debt, the statute has been reduced to three years.

State vs. City: If you're using a city, county, or state government in New York, there are different rules and shorter time limits. Often, you must file a notice of claim within 90 days of the event.

Revival of Time-Barred Claims: In some unique situations, New York has allowed the revival of time-barred claims, especially in cases of child sexual abuse. The Child Victims Act, for instance, opened a window for older claims to be brought.

Ignorance isn't Bliss: Not knowing about the statute of limitations is typically not an excuse that will be accepted in court. It's vital to act promptly if you believe you have a claim.

18) Can a debt collector get me to sign away my statute of limitations defense after I've defaulted on a credit card or consumer debt?

Yes, under GOB § 17-103, a debt collector could ask you to sign a written waiver of the statute of limitations defense after your cause of action has accrued (after you defaulted). However, this must be in writing and signed by you. Be very cautious about signing such documents - once you waive this defense in writing, you're giving the collector more time to sue you, essentially resetting the clock as if the debt just occurred.

19) If I make a payment on an old debt, does that waive my statute of limitations defense?

No! This is a crucial protection under New York law. Under New York's Consumer Credit Fairness Act (CPLR § 214‑i), effective April 7, 2022, ensures that once three years have passed since the default, **any subsequent payment or acknowledgment—written or oral—**cannot revive or extend that limitations period. However, you could still separately sign a written waiver under GOB § 17-103, so be careful about signing any documents when dealing with old debts.

20) What are some outstanding books about money management?

Okay, this is unrelated to the statute of limitations. But it's an extra. Here are 10 Phenomenal Books for the Money Conscious. One of those books was written by Dave Ramsey, and his blog recommends much of the same advice given here.

As always, contact us anytime you have questions. Learn about 7 Powerful Lawsuit Defenses for New York Debtors in 2023 (Consumer Credit Fairness Act).

Quiz: Understanding Statutes of Limitations

Questions

What is the statute of limitations for consumer credit transactions in New York as of April 7, 2022?

- A) 6 years

- B) 4 years

- C) 3 years

- D) 2 years

For how long are judgments in New York enforceable upon entry?

- A) 10 years

- B) 15 years

- C) 20 years

- D) 25 years

Which of the following is NOT a reason for the purpose of the statute of limitations?

- A) To promote justice

- B) To prevent stale, unreliable evidence

- C) To encourage prompt action

- D) To allow indefinite lawsuits

How long do late payments stay on your credit report?

- A) 5 years

- B) 7 years

- C) 10 years

- D) Indefinitely

When does the statute of limitations for credit card debt begin in New York?

- A) After the first purchase

- B) After the last payment

- C) When you miss a minimum payment

- D) When the account is closed

Are civil judgments included in credit reports after July 1, 2017?

- A) Yes, in all cases

- B) No

- C) Yes, but only partially

- D) Only for certain types of judgments

What happens if you make a payment on an old, time-barred debt?

- A) It has no effect on the statute of limitations

- B) It extends the credit reporting period

- C) It restarts the statute of limitations

- D) It clears the debt entirely

What was the effect of Executive Order No. 202.8 during the Covid-19 pandemic on statutes of limitations in New York?

- A) Extended indefinitely

- B) Suspended from March 20, 2020, to November 3, 2020

- C) Reduced by half

- D) No effect

Which bank does NOT use a three-year statute of limitations under Delaware law for their credit-card agreements?

- A) Chase

- B) Bank of America

- C) Citibank

- D) Barclays

What triggers the statute of limitations for medical debt in New York?

- A) Date of the last payment

- B) Date of the first symptom

- C) Date of treatment

- D) Date of diagnosis

Answer Key

- C) 3 years

- C) 20 years (The judgment lien on real property lasts only 10 years unless renewed under CPLR § 5014.)

- D) To allow indefinite lawsuits

- B) 7 years

- C) When you miss a minimum payment

- B) No

- C) It restarts the statute of limitations

- B) Suspended from March 20, 2020, to November 3, 2020

- C) Citibank

- C) Date of treatment

More Case Summaries

Contract Claims by Non-Residents Accrue at Place of Economic Injury Under NY Borrowing Statute

A consulting firm sought over $9 million in fees for services rendered under a 1988 contract. The court held that under New York's borrowing statute (CPLR 202), the plaintiff's contract and quantum meruit claims accrued where it sustained economic injury - its state of residence - rather than New York where the contract was negotiated, performed, and allegedly breached. Because the plaintiff was a non-resident corporation and its claims were time-barred in both Delaware (its state of incorporation) and Pennsylvania (its principal place of business), the action was dismissed.

Key Legal Principles:

- For purposes of CPLR 202, contract claims accrue where the plaintiff sustains the economic impact of the alleged breach

- When injury is purely economic, the place of injury is typically where the plaintiff resides

- The borrowing statute requires non-resident claims to be timely under both New York's statute of limitations and that of the jurisdiction where the cause of action accrued

Conclusion: The decision establishes a clear rule that prioritizes the plaintiff's residence over the location of contractual activities when determining where a cause of action accrues under New York's borrowing statute, promoting certainty and uniform application.

Citation: Global Fin Corp v Triarc Corp, 93 NY2d 525 (1999).

COVID-19 Executive Orders Toll Statute of Limitations in Credit Card Debt Action Despite Foreign State's Different Tolling Rules

A debt buyer sought to recover approximately $4,600 in credit card debt purchased from Citibank. The court granted summary judgment to the plaintiff, holding that New York's COVID-19 executive orders tolling the statute of limitations applied even though South Dakota (where the cause of action accrued) had different tolling provisions. The case notably addressed the intersection of New York's borrowing statute and emergency COVID-19 tolling measures.

Key Legal Principles:

- When a nonresident sues on a cause of action accruing outside New York, the action must be timely under both New York and the jurisdiction where the cause of action accrued

- Credit card statements showing card usage can establish a debt obligation even without the original agreement

- New York's COVID-19 executive orders tolling civil deadlines from March 20, 2020 through November 3, 2020 apply to actions filed in New York courts regardless of where the cause of action accrued

Conclusion: This decision establishes that New York's COVID-19 tolling orders can extend the statute of limitations for debt collection actions filed in New York courts, even when the underlying cause of action accrued in a state with different emergency measures.

Citation: Cavalry SPV I, LLC v King, 72 Misc 3d 980 (Civ Ct, NY County 2021).

[1] CPLR § 213. Actions to be commenced within six years: where not otherwise provided for; on contract; on the sealed instrument; on bond or note, and mortgage upon real property; by state based on misappropriation of public property; based on mistake; by the corporation against director, officer or stockholder; based on fraud

The following actions must be commenced within six years:

1. an action for which no limitation is specifically prescribed by law;

2. an action upon a contractual obligation or liability, express or implied, except as provided in section two hundred thirteen-a of this article or article 2 of the uniform commercial code or article 36-B of the general business law;

3. an action upon a sealed instrument;

4. an action upon a bond or note, the payment of which is secured by a mortgage upon real property, or upon a bond or note and mortgage so secured, or upon a mortgage of real property, or any interest therein;

5. an action by the state based upon the spoliation or other misappropriation of public property; the time within which the action must be commenced shall be computed from discovery by the state of the facts relied upon;

6. an action based upon mistake;

7. an action by or on behalf of a corporation against a present or former director, officer or stockholder for an accounting, or to procure a judgment on the ground of fraud, or to enforce a liability, penalty or forfeiture, or to recover damages for waste or for an injury to property or for an accounting in conjunction therewith.

8. an action based upon fraud; the time within which the action must be commenced shall be the greater of six years from the date the cause of action accrued or two years from the time the plaintiff or the person under whom the plaintiff claims discovered the fraud, or could with reasonable diligence have discovered it.

9. an action by the attorney general pursuant to article twenty-three-A of the general business law or subdivision twelve of section sixty-three of the executive law.

CPLR 213

[2] Executive Order No. 202.8 (based on a declaration of disaster): “any specific time limit for the commencement, filing, or service of any legal action, notice, motion, or other process or proceeding, as prescribed by the procedural laws of the state, including but not limited to the criminal procedure law, the family court act, the civil practice law and rules, the court of claims act, the surrogate’s court procedure act, and the uniform court acts, or by any other statute, local law, ordinance, order, rule, or regulation, or part thereof, is hereby tolled from the date of this executive order until April 19, 2020…”