What are your rights when your bank account is jointly held? Can the creditor's attorney simply take all of the money?

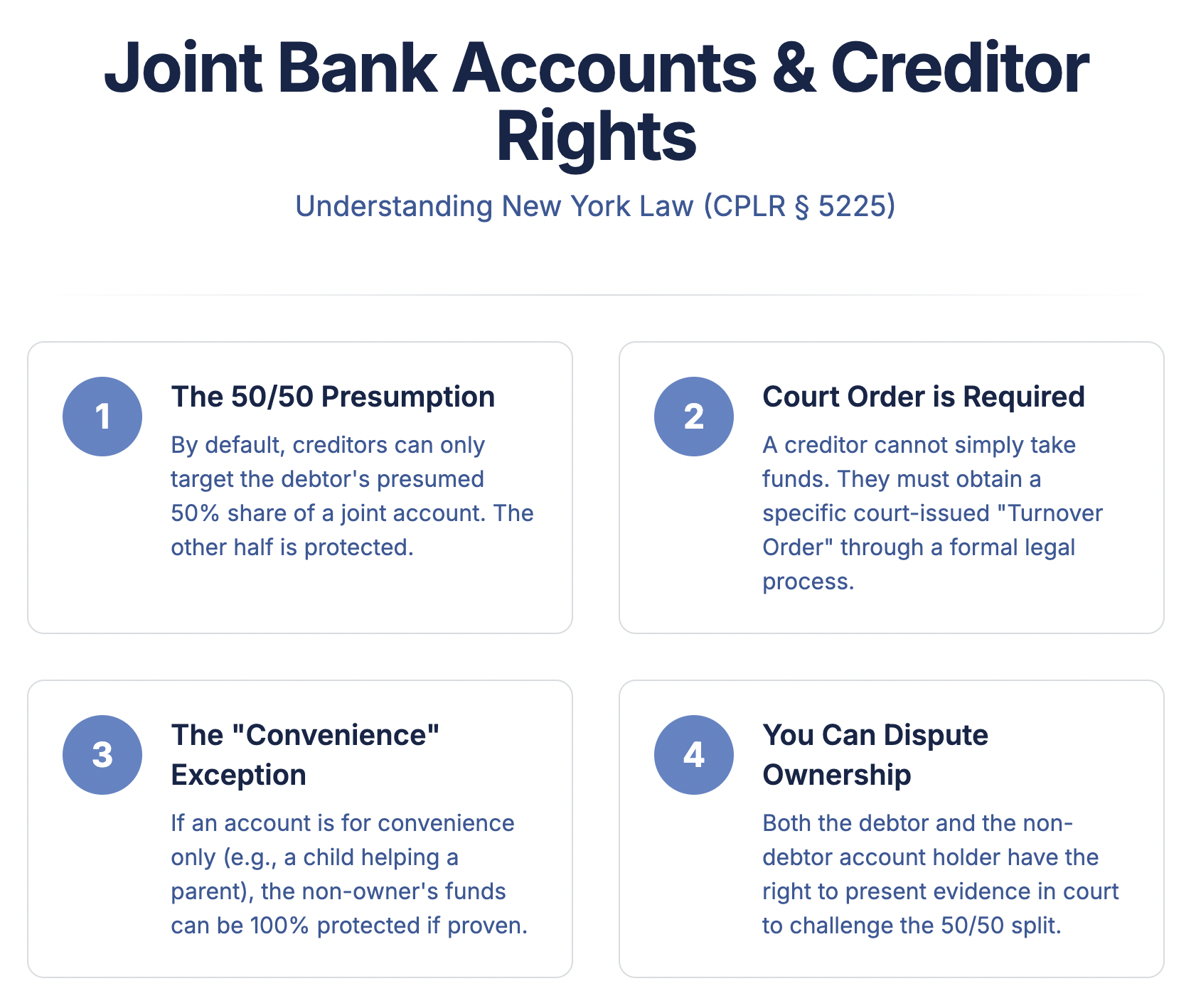

Under New York law, a joint bank account generally creates a presumption that each holder owns 50% of the funds, unless evidence shows otherwise. Because of this presumption, a creditor must obtain a court-issued ‘turnover order’ before funds in a joint account can be released. Other reasons exist to obtain a turnover order, for example, when a debtor or garnishee fails to honor an execution. The process is set forth below, which summarizes New York CPLR § 5225. This blog entry is part of our series to summarize each section of New York Article 52 relating to the enforcement of money judgments.

Joint Bank Accounts & Creditors in New York: A Deeper Look

NY Banking Law Basics

In New York, joint accounts have specific protections when creditors try to freeze or seize funds:

Presumption of 50% Access

- By default, creditors may reach the debtor’s presumed 50% share of joint account funds, unless evidence shows a different ownership interest

- Example: In a $10,000 joint account, creditors can only freeze/seize $5,000

- Based on assumption each owner has equal rights to funds

Convenience Accounts (Banking Law 678-a)— Accounts where one person adds another for convenience, without granting ownership rights

- Special designation where one person owns all money but adds another for practicality

- Examples:

- Adult child added to elderly parent's account

- Spouse added for bill-paying purposes

- Caregiver added for shopping assistance

Proving Convenience Status

Must show evidence like:

- Only one person deposits funds

- Second person never uses ATM/debit card

- No withdrawals by second person

- Bank statements showing single-person usage

- Bank letter confirming convenience arrangement

Banking Law 675 Protection

- Creates presumption of 50/50 ownership

- If ownership is disputed, the burden may shift: creditors must prove the debtor owns more than 50%, while non-debtors must prove they own more than their presumed share

- Protects non-debtor's share of funds

- Example: If creditor believes debtor owns 75%, they must prove it in court

Key Evidence to Gather

- Account statements showing deposit sources

- ATM/debit card records

- Check writing history

- Bank account opening documents

- Written agreements between account holders

Pro Tip: When opening joint accounts in NY, clearly document if it's for convenience to prevent future creditor issues.

Collection on the Joint Account

The Creditor Finds Assets

After a judgment for a debt has been entered, a creditor will investigate to see if it can discover money or property that the debtor owns that could be used to satisfy the debt. We've discussed this investigation process, called disclosure, in other posts on this blog. Now, let's discuss what happens when a creditor finds assets and how they go about obtaining them from a debtor or bank or whoever is holding the debtor's money.

The Turnover-Order Process under CPLR §5225

If a creditor finds money or property and thinks it can be claimed to satisfy the debt, it will probably seek a court order to have the money or property turned over. The process for this is outlined in New York CPLR §5225 and is explained below.

A creditor will make a motion to identify the money or property, explaining why it is available to satisfy the debt and requesting that the court order the money or property to be turned over. Notice of the motion must be served on the debtor either in the same manner as a summons or by registered/certified mail with return receipt requested. The court can either order the debtor or someone else, to turn over assets:

- Debtor. If the money or property is in the debtor's possession and the court is satisfied with the creditor's motion, the court will order the debtor to turn over a sufficient amount of money or property to satisfy the debt. If the court grants the motion, it may direct the sheriff or another enforcement officer to collect the funds or property.

- Someone Else. If the money or property is in the possession of someone other than the debtor, the motion must be served not only on the debtor but on whoever it is the creditor claims has the money or property.

The motion needs to explain why the creditor believes the money or property belongs to the debtor and also show that the creditor has a higher priority interest in the money or property than the person holding it. The debtor can speak up if he or she disagrees. The debtor may oppose the motion, and third parties claiming an interest may intervene in the proceeding. Once the court has heard from everyone with interest, it will decide whether the creditor can claim any of the money or property and, if so, will designate a sheriff to receive the money or property and order that it be turned over.

In rare cases, the court may award costs against a debtor or intervenor if it finds their claims were frivolous or caused undue delay. However, the court can't award costs against a party who receives a motion to turn over money or property because they didn't dispute the debtor's right to the money or property.

If you have questions about court orders for payment of money or property to a creditor, contact an attorney for advice right away. Understanding your rights and obligations under the law is important before taking any action.

See this page for a more thorough analysis of bank restraints and exemptions. Many of our clients contact us after one of the following debt collectors has frozen their bank accounts. Here's a blog entry as to how it happened.

Summary of Turnover Practice

- New York law dictates that a "turnover order" must be secured by creditors to access funds in a jointly-held bank account, as both account holders have an equal and unconditional right to half of the money.

- In instances where a debtor or garnishee fails to respect an execution, as defined by New York CPLR § 5225, a turnover order becomes necessary.

- Following a debt judgment, creditors perform a disclosure process to locate the debtor's assets that could potentially be used for debt clearance.

- When assets are found and deemed suitable for debt settlement, creditors may apply for a court order to have these assets turned over.

- To do this, creditors need to file a motion in court specifying the assets, justifying their availability for debt settlement, and petitioning the court to order its turnover. This motion must be served to the debtor.

- The court may direct the debtor or a third party who holds the debtor's assets to surrender them. Usually, a sheriff is appointed to collect the assets from the debtor.

- If the assets are held by a third party, the motion must be served to both the debtor and this third party. After hearing all parties, the court decides if the creditor has a claim over any of the assets.

- The court can impose costs on a debtor or an intervening party if they are found to be causing unnecessary delays without a valid claim.

![]()

Summary of the Legal Elements of CPLR § 5225

Below are key points summarizing the requirements of CPLR § 5225:

Possession of Property by Judgment Debtor: When it is demonstrated that the judgment debtor holds money or personal property, the court, upon motion by the judgment creditor, may order the judgment debtor to pay sufficient funds to satisfy the judgment or deliver valuable personal property to a designated sheriff.

Notice to Judgment Debtor: The motion to obtain payment or delivery must include notice to the judgment debtor, which can be served in a manner similar to a summons or through registered or certified mail with return receipt requested.

Property Not in the Possession of Judgment Debtor: If the property is not in the possession of the judgment debtor but is held by another person, the judgment creditor may initiate a special proceeding against that person. This applies to situations where the judgment debtor has an interest in the property, or the creditor's rights to the property are superior to the transferee's rights.

Payment and Delivery Orders: In such proceedings, the court may require the third party to pay sufficient funds or deliver personal property to satisfy the judgment. The judgment debtor is also served with notice of this proceeding in a manner similar to a summons or through registered or certified mail.

Intervention: The judgment debtor may be permitted to intervene in the special proceeding, and the court can decide on the rights of any adverse claimants.

Execution of Documents: The court has the authority to order any person to execute and deliver necessary documents to facilitate payment or delivery as required by the judgment.

Understanding CPLR § 5225 is crucial for judgment creditors seeking to enforce judgments and debtors who may be subject to these legal proceedings.

10 Things Consumers Should Know about Turnover Proceedings Against Joint Bank Accounts

Definition of Turnover Proceedings: Turnover proceedings involve a legal process by which a judgment creditor seeks to collect a debt by accessing funds held in a bank account. In the case of joint bank accounts, this includes accounts held by two or more individuals.

Joint Account Ownership Matters: Joint bank accounts typically have multiple account holders, and each account holder has equal rights to the funds in the account. However, this joint ownership can complicate the process of accessing funds through turnover proceedings.

Rights of Individual Account Holders: In true joint accounts, each holder has equal access and use rights. In contrast, in convenience accounts, the added person has access but no ownership interest.

Creditor's Rights: If a judgment has been entered against one of the joint account holders, a judgment creditor may seek to access the funds in the joint account to satisfy the debt. However, the creditor's ability to do so may be limited.

Exemptions: State laws often provide exemptions that protect certain funds in a joint account from being used to satisfy a debt. These exemptions can vary widely by jurisdiction and may protect specific types of funds, such as Social Security benefits, child support, or public assistance.

Burden of Proof: To access funds in a joint account, the judgment creditor typically needs to prove that the funds belong to the debtor against whom the judgment was entered. This may require documentation and evidence.

Notification: In many cases, both account holders are entitled to notice of the turnover proceedings. This means that the non-debtor account holder may become aware of the situation.

Potential Disputes: Turnover proceedings involving joint accounts can lead to disputes between account holders. The non-debtor account holder may object to the seizure of funds or claim that they belong to them and not the debtor.

Legal Assistance: Consumers facing turnover proceedings should seek legal advice and representation. An attorney can help protect their rights and explore legal options, including exemptions that may apply.

Alternatives to Joint Accounts: To avoid potential complications related to joint account seizures, consumers may consider maintaining separate accounts or exploring other financial arrangements that protect their assets in case of legal disputes.

Important Legal Precedents: Bank Accounts, Insurance, and Receivables

Bank Accounts:

Canadian bank lacked "possession or custody" over judgment debtor's Cayman Islands bank accounts, New York law didn't authorize a post-judgment turnover order. Northern Mariana Islands v. Canadian Imperial Bank of Commerce, 717 F.3d 266 (2d Cir. 2013).

Blocked electronic funds transfers (EFTs) to Cuban beneficiaries held in New York banks were not "assets" subject to attachment under terrorism-related regulations. Martinez v. Republic of Cuba, 149 F. Supp. 3d 469 (S.D.N.Y. 2016).

Funds possessed by a New York bank, blocked pursuant to Presidential Executive Orders, could be attached to satisfy a judgment against Iran and Iran-based entities. Estate of Heiser v. Bank of Tokyo Mitsubishi UFJ, N.Y. Branch, 919 F. Supp. 2d 411 (S.D.N.Y. 2013).

Invalid application for enforcement of judgment against a joint bank account due to noncompliance with service requirements. Long Island Jewish Med. Ctr. v. Sovereign Bank, 15 Misc. 3d 1041, 838 N.Y.S.2d 413 (Sup. Ct. Queens Cnty. 2007).

Judgment creditor entitled to full amount of funds in a joint bank account when both parties were served with turnover application. Ford Motor Credit Co. v. Astoria Federal, 189 Misc. 2d 475, 733 N.Y.S.2d 583 (Dist. Ct. Nassau Cnty. 2001).

Default by non-debtor co-tenant in a joint bank account turnover proceeding allows the creditor to access the entire account. In some cases, such as Ford Motor Credit Co. v. Astoria Federal (2001), a non-debtor’s default allowed the creditor to reach the entire account. However, later cases have applied this more cautiously, preserving the non-debtor’s rights where possible. Ford Motor Credit Co. v. Astoria Federal, 189 Misc. 2d 475, 733 N.Y.S.2d 583 (Dist. Ct. Nassau Cnty. 2001).

Judgment creditor can reach the whole joint bank account when default rebuts the presumption of equal ownership. Ford Motor Credit Co. v. Astoria Federal, 189 Misc. 2d 475, 733 N.Y.S.2d 583 (Dist. Ct. Nassau Cnty. 2001).

Wife entitled to receive balance of husband's bank account used for business commissions to satisfy maintenance arrears. Freeman v. Freeman, 119 Misc. 2d 775, 464 N.Y.S.2d 676 (Sup. Ct. Oneida Cnty. 1983).

Failure of one bank to appear in interpleader action doesn't affect its status regarding priorities claimed by other claimants. County Nat. Bank v. Inter-County Farmers Co-op. Ass'n, 65 Misc. 2d 446, 317 N.Y.S.2d 790 (Sup. Ct. Sullivan Cnty. 1970).

Under CPLR 5222-a, banks must provide debtors with exemption notices and claim forms when serving a restraining notice, ensuring the debtor’s opportunity to assert exemptions. North Shore Univ. Hosp. at Plainview v. Citibank Legal Serv. Intake Unit, 25 Misc. 3d 655, 883 N.Y.S.2d 898 (Dist. Ct. Nassau Cnty. 2009).

Judgment debtor's bank deposit couldn't be ordered to be paid to the sheriff in a supplementary proceeding under certain statutes. Chanin Realty Corp. v. U.S. Bond & Mortg. Corp., 146 Misc. 658, 262 N.Y.S. 600 (City Ct. N.Y.C. 1933).

Bank couldn't be required to deliver judgment debtor's money on deposit to the sheriff for the purpose of paying a judgment. Capital City Sur. Co. v. De Luxe Sightseeing Co., 133 Misc. 750, 233 N.Y.S. 126 (City Ct. N.Y.C. 1927).

Default in appearance of a non-judgment debtor in a turnover proceeding doesn't entitle the court to award the judgment creditor more than half of the account. Direct Merchants Credit Card Bank v. Greenpoint Bank, 2003 WL 2004163 (Dist. Ct. Nassau Cnty. Mar. 11, 2003).

Receivables:

- Future rents not considered tangible property or debt subject to levy. (Neshewat v. Salem, 2005, 365 F.Supp.2d 508)

Line of Credit:

- Judgment debtor's credit card line of credit wasn't assignable or transferable property. (Carbo Industries, Inc. v. Alcus Fuel Oil, Inc., 2014, 46 Misc.3d 726, 998 N.Y.S.2d 571)