If you settled a judgment for less than the full amount, the IRS may treat the forgiven portion as taxable income — unless the settlement reflects a bona fide dispute over the amount or enforceability of the debt, or a statutory exclusion applies. Many people who settle owe nothing — but you need to understand the rules to protect yourself.

Is the forgiven part of a judgment settlement taxable?

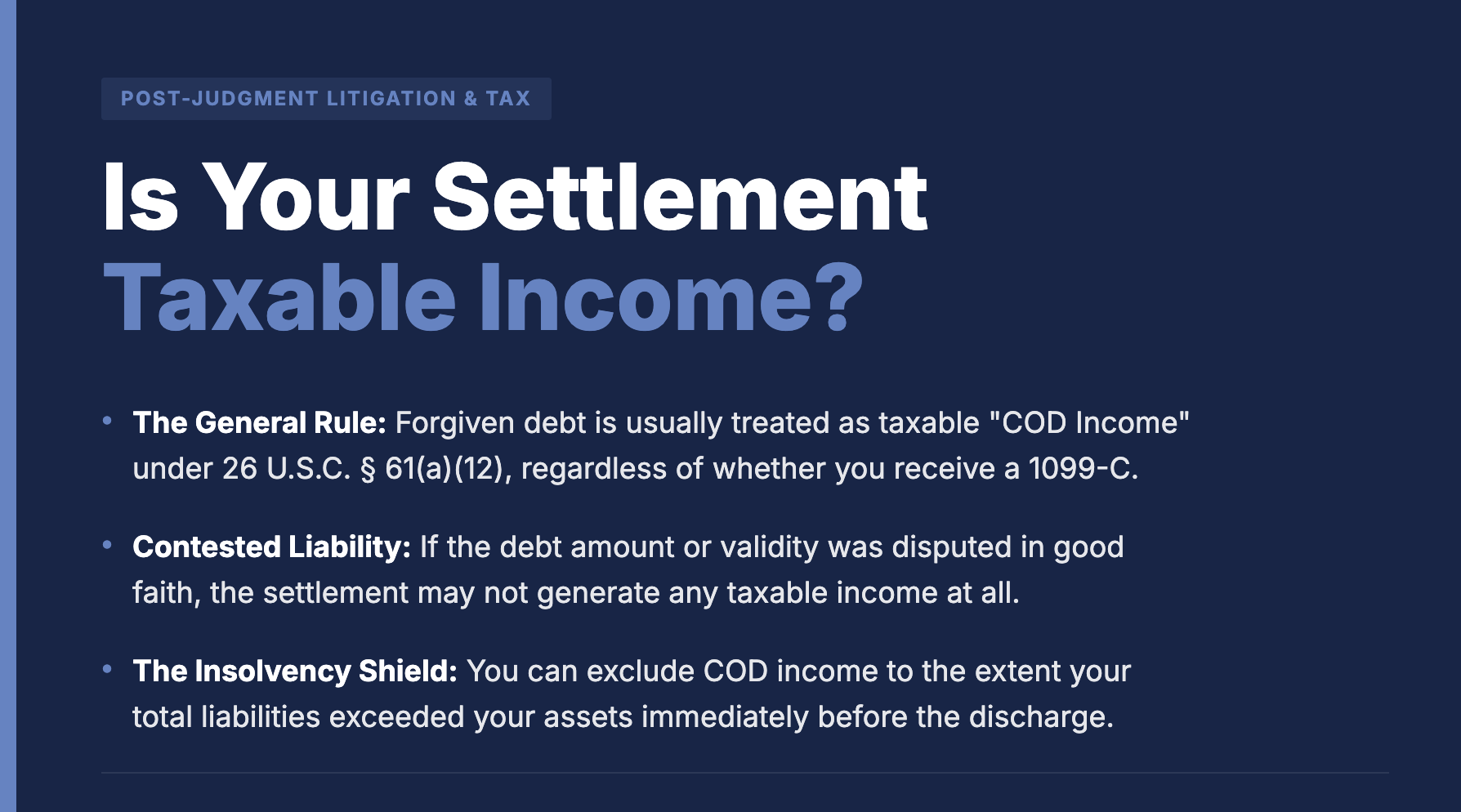

It can be. Under 26 U.S.C. § 61(a)(12), gross income includes "income from discharge of indebtedness." Treasury Regulation § 1.61-12 reinforces that a discharge of indebtedness "in whole or in part, may result in the realization of income."

If you owed $100,000 under a final and undisputed judgment and settled for $40,000, the $60,000 difference is generally treated as cancellation-of-indebtedness (COD) income — unless a statutory exclusion applies or the settlement reflects a bona fide dispute over the amount or enforceability of the debt.

This is true regardless of who the creditor is. Neither § 61(a)(12) nor Treasury Regulation § 1.61-12 limits COD income to debts held by banks or financial institutions. The focus is on the economic event: an enforceable obligation that is treated as due has been reduced or cancelled. Whether the judgment is held by a bank, a debt buyer, a former landlord, or a private individual, the discharge of part of that judgment can produce COD income.

For New York residents, the state tax consequences generally follow federal. New York Tax Law § 612 begins with federal adjusted gross income. In most cases, COD income included in federal AGI flows through to New York AGI unless a specific state modification applies.

Do I have to pay taxes if I never received a 1099-C?

Yes, potentially. The 1099-C filing requirement under 26 U.S.C. § 6050P applies only to certain "applicable entities" — banks, credit unions, federal agencies, and entities with a significant trade or business of lending money. Many judgment creditors — such as individual landlords or private parties not engaged in a significant trade or business of lending money — may have no obligation to file a 1099-C.

Even among creditors who must file, the rules are narrower than most people assume. Reporting is generally required only when the amount required to be reported meets the $600 threshold, and the regulations determine what portions of the debt must be reported in different contexts. But:

- Treasury Regulation § 1.6050P-1(d)(2) exempts discharged interest from the reporting requirement.

- Section 1.6050P-1(d)(3) provides that in lending transactions, only discharged stated principal must be reported.

In Kaff v. Nationwide Credit, Inc., 2015 WL 12660327, at *3-5 (E.D.N.Y. 2015), a federal district court interpreted these provisions and concluded that in a lending transaction, reporting is required only when at least $600 in stated principal is discharged — not $600 in total indebtedness including interest and fees. The court relied on IRS Information Letter 2005-0208, which confirmed that in lending transactions, the reporting obligation applies only to stated principal. Id. at *4-5.

But here is the critical point: the tax obligation is independent of the form. Your duty to report COD income exists under § 61(a)(12) whether or not any creditor sends you paperwork. A creditor's failure to file a 1099-C — whether because it falls below the $600 principal threshold, because it is not an "applicable entity," or for any other reason — does not eliminate the debtor's income.

No 1099-C does not mean no tax.

The reverse is also true: receiving a 1099-C does not mean you automatically owe tax. The form is an information report. You can still claim exclusions under § 108.

Does a 1099-C mean the judgment is gone?

No. This is the most dangerous misconception, and both federal and New York appellate authority reject it.

In FDIC v. Cashion, 720 F.3d 169 (4th Cir. 2013) — the leading federal appellate decision on point — the debtor argued that a creditor's filing of a Form 1099-C constituted prima facie evidence that the debt had been cancelled. The Fourth Circuit disagreed, holding that the 1099-C "does not, standing alone, constitute sufficient evidence that a debt has been cancelled." Id. at 180.

The court explained that the IRS "treats the Form 1099-C as a means for satisfying a reporting obligation and not as an instrument effectuating a discharge of debt or preventing a creditor from seeking payment on a debt." Id. at 179. Because a creditor can be required to file a 1099-C even where no actual discharge has occurred — triggered by events such as 36 months of non-payment or a decision to discontinue collection activity — the form standing alone tells a court nothing definitive about the status of the debt. Id. at 178-80.

New York follows the same principle. In Bank of America, N.A. v. Rolf, 188 A.D.3d 770, 136 N.Y.S.3d 124 (2d Dep't 2020), the mortgagee filed a 1099-C listing the debtor's name and reporting the deficiency amount as "discharged," then moved for a deficiency judgment. The debtor argued waiver and equitable estoppel. The Second Department rejected both arguments, holding that the filing "did not constitute a waiver of the plaintiff's right to seek a deficiency judgment" because the creditor "was required to file the form in order to satisfy a reporting obligation," and "it was clear from the actions of the plaintiff that it had not forgiven any part of the loan and had no intention of doing so." Id. at 773-74.

The takeaway is important: filing a 1099-C does not by itself prevent a creditor from continuing collection efforts unless the underlying debt has actually been released or satisfied. The form is a tax document. It is not a satisfaction of judgment, not a release, and not a vacatur.

If you receive a 1099-C on an unsettled judgment, do not assume the matter is resolved. Confirm whether a satisfaction of judgment has been filed under CPLR § 5020 before treating the obligation as extinguished.

Can I avoid COD income entirely?

There are two paths. Which one applies depends on the nature of the underlying debt and your financial circumstances.

Path 1: The Contested Liability Doctrine — No COD Income Exists

If the underlying debt was genuinely disputed, the settlement may not create COD income in the first place. Under the contested liability doctrine, when a debtor in good faith disputes the amount or existence of a debt, the settlement amount is treated as the true amount of the obligation. There is no "forgiven" portion because the liability was never fixed.

The leading appellate statement of the doctrine is Zarin v. Commissioner of Internal Revenue, 916 F.2d 110 (3d Cir. 1990). There, the taxpayer owed a casino $3,435,000 in gambling debts extended in violation of New Jersey credit regulations. The taxpayer disputed liability on enforceability grounds, and the parties settled for $500,000. The IRS argued that the $2,935,000 difference constituted cancellation of indebtedness income under §§ 61(a)(12) and 108.

The Third Circuit reversed the Tax Court and held that no income was recognized. The court explained:

"if a taxpayer, in good faith, disputed the amount of a debt, a subsequent settlement of the dispute would be treated as the amount of debt cognizable for tax purposes. The excess of the original debt over the amount determined to have been due is disregarded for both loss and debt accounting purposes." Id. at 115.

The $500,000 settlement "fixed the amount of loss and the amount of debt cognizable for tax purposes," and when the taxpayer paid it, "no adverse tax consequences attached." Id. at 116.

The doctrine applies when the dispute goes to what was actually owed or whether the obligation is enforceable. In the debt collection context, examples include:

- The creditor claims $100,000 but the debtor has a good-faith basis to argue the real figure is lower (inflated interest, disputed charges, usury).

- The creditor's standing or chain of title is contested.

- The debtor disputes owing anything to that particular entity.

The key requirement is a bona fide dispute — not a strategic disagreement manufactured at settlement, but a genuine controversy about the amount or validity of the underlying obligation.

The language of the settlement agreement matters. If the stipulation recites the substantive disputes about the debt — the amount claimed, the creditor's right to collect, defenses to the underlying obligation — it supports the position that the settlement resolved a contested claim rather than discounted a fixed debt. If the stipulation is silent on these issues, the IRS is more likely to treat the difference as classic COD income.

Path 2: The Insolvency Exclusion — COD Income Exists but Is Not Taxable

Under 26 U.S.C. § 108(a)(1)(B), you can exclude COD income to the extent you were insolvent immediately before the discharge. Insolvent means your total liabilities exceeded the fair market value of your total assets.

For many judgment debtors, insolvency may eliminate all or most COD income — but this depends on a careful balance-sheet analysis. Inability to pay a judgment does not automatically establish insolvency. Insolvency under § 108(d)(3) requires that your total liabilities exceed the fair market value of your total assets immediately before the discharge. That said, the judgment itself is often the largest liability on the balance sheet, and debtors who settled precisely because they could not pay are frequently insolvent by this measure.

The calculation: list every asset at fair market value (including retirement accounts, even if they are exempt from creditors) and every liability (the full pre-settlement judgment amount, plus all other debts). If liabilities exceed assets by more than the COD amount, the entire amount is excluded.

Example: You settle a $150,000 judgment for $50,000. COD income: $100,000. Your assets total $80,000 and your liabilities total $250,000. You are insolvent by $170,000 — more than the $100,000 of COD income — so the entire COD amount may be excluded, subject to required tax attribute reductions under § 108(b).

You must file IRS Form 982 with your return for the year of the settlement to claim this exclusion. It does not apply automatically. Failing to file Form 982 is the most common and most expensive mistake judgment debtors make — the IRS may match the 1099-C to your return, see no corresponding treatment, and issue a CP2000 underreporter notice.

Other Exclusions

The bankruptcy exclusion under § 108(a)(1)(A) is unlimited and takes priority over all other exclusions.

The qualified principal residence indebtedness exclusion under § 108(a)(1)(E) reflects a policy judgment that homeowners forced into foreclosure, short sale, or loan modification should not face an additional tax bill on the forgiven mortgage balance. Congress enacted this provision through the Mortgage Forgiveness Debt Relief Act of 2007 in direct response to the subprime mortgage crisis. The concern was straightforward: a homeowner who loses a home and has $200,000 of mortgage debt forgiven is in no position to pay taxes on $200,000 of phantom income.

Key limitations:

- Applies only to acquisition indebtedness on a principal residence (not home equity lines used for other purposes).

- Capped at $750,000 ($375,000 married filing separately).

- As currently enacted, the exclusion applies to discharges occurring on or before December 31, 2025 (or pursuant to certain written agreements entered before that date). Absent further legislation, it does not apply to later discharges. 26 U.S.C. § 108(a)(1)(E).

Congress extended this provision eight times between 2007 and 2020, but as of this writing, no further extension has been enacted — likely because the combination of a recovered housing market, diminished foreclosure volume, the availability of the insolvency exclusion as a backstop, and the revenue cost of renewal made the political case for extension weaker than in prior cycles.

The qualified real property business indebtedness exclusion under § 108(a)(1)(D) serves a different policy: keeping commercial real estate operators solvent during downturns. When a business property declines in value below its mortgage balance and the lender agrees to reduce the principal, the borrower would otherwise face COD income at the worst possible time — when the property that secures the debt has already lost value.

Key limitations:

- Applies only to non-corporate taxpayers and requires an election.

- Excluded amount cannot exceed the excess of the outstanding principal over the fair market value of the securing property. 26 U.S.C. § 108(c)(2)(A).

- The taxpayer must reduce the basis of depreciable real property by the excluded amount. 26 U.S.C. § 108(c)(1).

- Unlike the principal residence exclusion, this provision is permanent and has no sunset date.

What should I do before, during, and after settling a judgment?

What should I do before, during, and after settling a judgment?

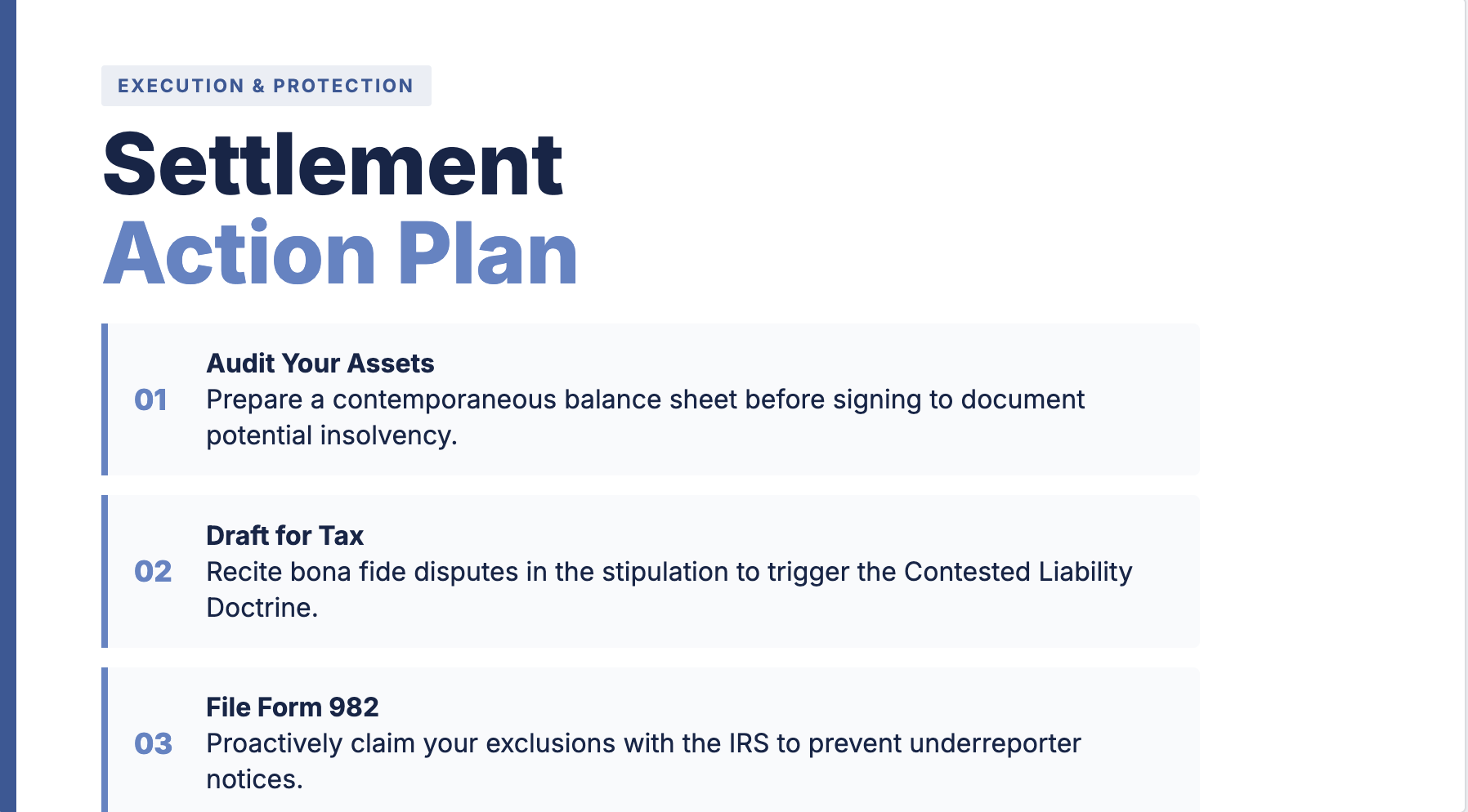

Before: Determine whether you are insolvent under 26 U.S.C. § 108(d)(3) — meaning your liabilities exceed the fair market value of your assets immediately before the discharge. If you are, you may exclude some or all COD income. But you must be ready to prove it.

The IRS places the burden of establishing insolvency on the debtor. The way you carry that burden is with a contemporaneous balance sheet prepared as of the settlement date. Do this before you sign the stipulation, not after.

During: Make sure the settlement agreement works for you on the tax side. The stipulation is a legal document — make it do legal work.

If there are legitimate disputes about the debt, have them recited in the stipulation. The contested liability doctrine requires evidence of a genuine dispute, not after-the-fact labeling. The stipulation should recite:

- That the amount or liability was bona fide disputed.

- That the settlement is in compromise of that dispute.

- That the parties treat the settlement amount as the actual debt for tax purposes.

Address the 1099-C directly:

- If you are relying on contested liability, the agreement should state that the settlement reflects a bona fide dispute and, to the extent the creditor determines it has no reporting obligation, that it does not anticipate issuing a Form 1099-C.

- If the creditor insists on reserving the right to issue one, the agreement should at minimum state that the settlement resolves a contested claim.

- Clear tax-treatment language can strengthen your position and reduce disputes, though the IRS ultimately applies federal tax law based on the underlying facts and economic substance.

Include a clause stating each party bears its own tax consequences. Commentary on attorneys' ethical obligations in settlement negotiations — grounded in the duty of competence and the duty to provide candid advice — recommends both alerting clients to potential tax implications and documenting that each party is responsible for its own tax treatment.

After: If you receive a 1099-C, file IRS Form 982 with your tax return to claim any applicable exclusion. Receipt of a 1099-C does not conclusively mean tax is owed — but you must address it.

If you do not receive a 1099-C, you are still required to report the COD income. The information return affects IRS matching and audit risk, not the existence of the income itself. You can exclude COD on the same return if you qualify.

Do not wait for the IRS to send a CP2000 underreporter notice. That process is significantly more burdensome than filing Form 982 proactively.

Satisfy the judgment separately. Confirm that the judgment creditor has filed a satisfaction of judgment under CPLR § 5020. Only a properly executed and filed satisfaction — or partial satisfaction — clears the judgment from the court's docket. A creditor's write-off or 1099-C does not accomplish this. Payment in full does not automatically clear the court record either; the creditor must file a satisfaction, and the debtor may move to compel if it is not filed. Federal tax reporting and state court enforcement are two separate systems.

This article is for informational purposes only and does not constitute tax or legal advice. Consult with a qualified tax professional regarding your specific situation.