In the high-stakes environment of New York City debt defense, waiting is often not a neutral strategy. Whether you are dealing with a major bank or a third-party debt collector, many people observe the current economic landscape—with elevated inflation and shifting interest rates—and conclude that there is no urgency. They think, "Why rush? I can just handle this later with cheaper dollars."

This is a common—and potentially expensive—misconception. In many cases, delay can reduce negotiating leverage—particularly where interest continues to accrue or litigation progresses. To be clear, where strong legal or evidentiary defenses exist, litigation should be pursued to protect your rights. However, when you weigh the reality of consumer debt litigation against the "Triple Stack" of financial advantages available in many cases, the financial tradeoffs in many cases are clear: Delaying a resolution where liability is likely or uncontested can effectively result in paying a premium for that debt later.

1. How Does Settling Now Save Me Money? (The "Triple Stack" Advantage)

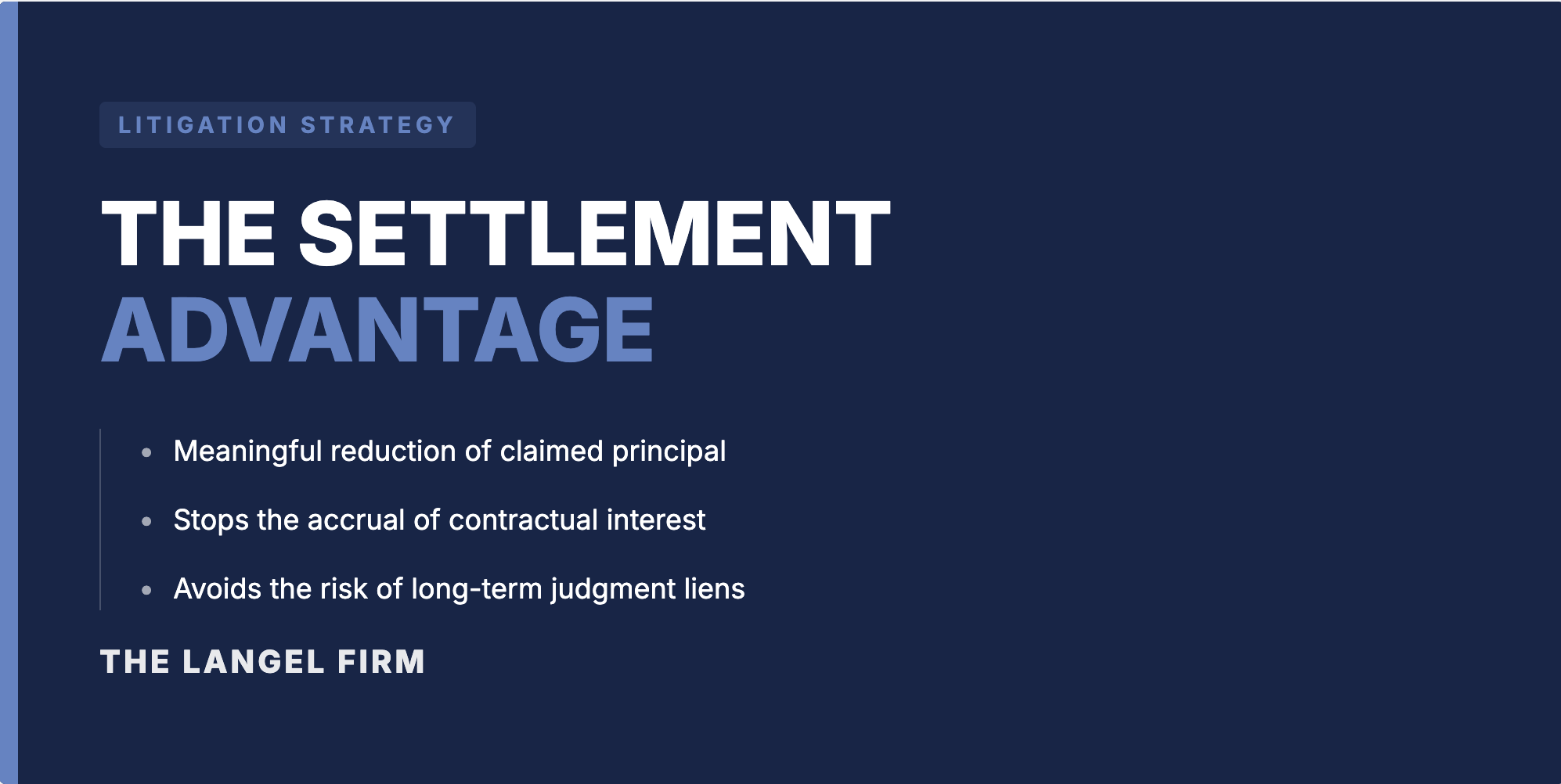

When we negotiate a resolution for you, we aren't just seeking a "discount." We are constructing a three-layered financial win that often evaporates once a case moves toward judgment.

Stack 1: Can I really reduce the principal amount? In many cases, yes. Depending on the creditor, the documentation, and the stage of the case, creditors are often willing to accept meaningful reductions—frequently in the range of 30–60%.

Stack 2: Can I stop the interest and legal fees from growing? In many cases, yes. While New York has a 2% rate for judgments on consumer debt, creditors may still seek contractual interest rates (which can exceed 20%), where permitted and adequately supported by the underlying agreement, for the period before the judgment is signed. Settling now stops the continued accrual of these costs.

Stack 3: Does inflation help me if I pay today? By locking in a fixed-dollar obligation today, you are effectively locking in today’s dollars against a fixed obligation. In an inflationary environment, you are repaying the creditor with dollars that have less purchasing power than the ones you originally borrowed.

2. What is the "Pre-Judgment Interest" Trap? (CPLR 5001 vs. 5004)

There is a significant misunderstanding regarding the "2% interest cap" in New York. To protect your assets, you must understand where that cap applies—and where it often doesn't.

Stage of Debt | Interest Law | Typical Rate |

|---|---|---|

Pre-Judgment (Default to Judgment) | CPLR 5001 | Contractual Rate (Often 20%+ if enforceable) |

Post-Judgment (Once signed by Court) | CPLR 5004 | 2% Capped Rate |

The Gap: New York’s 2% cap does not apply to interest accrued while the case is in court. Under CPLR 5001, creditors may seek interest from the "earliest ascertainable date" the cause of action existed—often tied to default or breach.

The Risk of Delay: If a lawsuit drags on for years, a creditor may seek to apply the contractual rate—sometimes exceeding 20%—though recovery depends on proving entitlement under the agreement and applicable law. By the time the 2% cap kicks in, the total claimed balance may have already grown significantly.

The Settlement Advantage: We often negotiate to reduce or eliminate claimed pre-judgment interest as part of a settlement, depending on the creditor and case posture.

3. Does it Matter Who is Suing Me? (Original Creditors vs. Debt Buyers)

The leverage we focus on depends heavily on who is suing you. New York law treats these entities differently, and we use those differences to your advantage.

What are the rules for all consumer debt in New York? (CPLR 3016-j)

New York law imposes specific pleading requirements under CPLR 3016(j), which can create leverage—particularly where documentation is incomplete or cannot be readily produced. The creditor must provide specific details in their complaint, including:

The name of the original creditor and an itemization of the amount sought.

For revolving accounts, a charge-off statement must be provided if the original contract is unavailable.

What if a major bank or my original lender is suing me?

Settlement opportunities are often most favorable when the creditor’s preference for certainty outweighs the costs of continued litigation. When a major bank or original lender sues you, the focus shifts to the point where their desire for a sure, front-loaded recovery beats the cost, delay, and uncertainty of pushing to judgment and enforcement.

Some lenders are under pressure to clear non-performing accounts from their books and will trade a discount for a lump-sum or accelerated payment schedule, especially where collection looks difficult or time-consuming. For example, if a lender doubts its practical ability to easily garnish wages or reach assets, it may agree to a reduced lump-sum payment in exchange for closing the file now rather than spending more on attorneys and court fees. Similarly, if a defendant has limited non-exempt income or property, the bank’s legal right to a judgment may be stronger than its practical ability to collect, which creates leverage to negotiate discounts or structured settlements.

Other institutions follow stricter internal policies and insist on pursuing the full claimed balance; however, even risk-averse institutions with rigid policies often prefer a realistic, documented deal today over years of litigation risk and enforcement battles.

What if my debt was sold to a "Debt Buyer"?

Debt buyers face potential challenges or delays if their documentation—specifically the "chain of title"—is incomplete. These evidentiary hurdles often create the necessary leverage to secure a favorable settlement.

4. Should I Use a Law Firm or a Debt Settlement Company?

Is there a risk in using a middleman? Yes. Debt settlement companies lack the legal authority to represent you in court. They often advise you to stop making payments, which can lead to lawsuits they cannot defend.

What is the "Law Firm Advantage"? Creditors often respond more favorably when a case is actively litigated by counsel. At The Langel Firm, we can promptly appear in the case and assert available defenses to challenge the creditor's evidence.

Why does a "Lump Sum" work better with a lawyer? Creditor attorneys know a deal with a law firm is legally sound and final. This certainty often makes them more receptive to meaningful reductions than they would be with a third-party agent.

5. Why Would the Creditor's Lawyer Agree to Take Less?

To win, you must understand the business model of the lawyers on the other side. They are managing a portfolio, not falling in love with an individual case.

Litigation as a Cost Center: Most collection firms are paid on contingency or flat-fee models. Every motion they draft and every court appearance they make chips away at their profit margin. Once we contest the case, your file becomes "overhead" for them.

The Need for Speed: Creditors measure these firms on speed of recovery. Offering a settlement helps them hit the "velocity" metrics their clients demand.

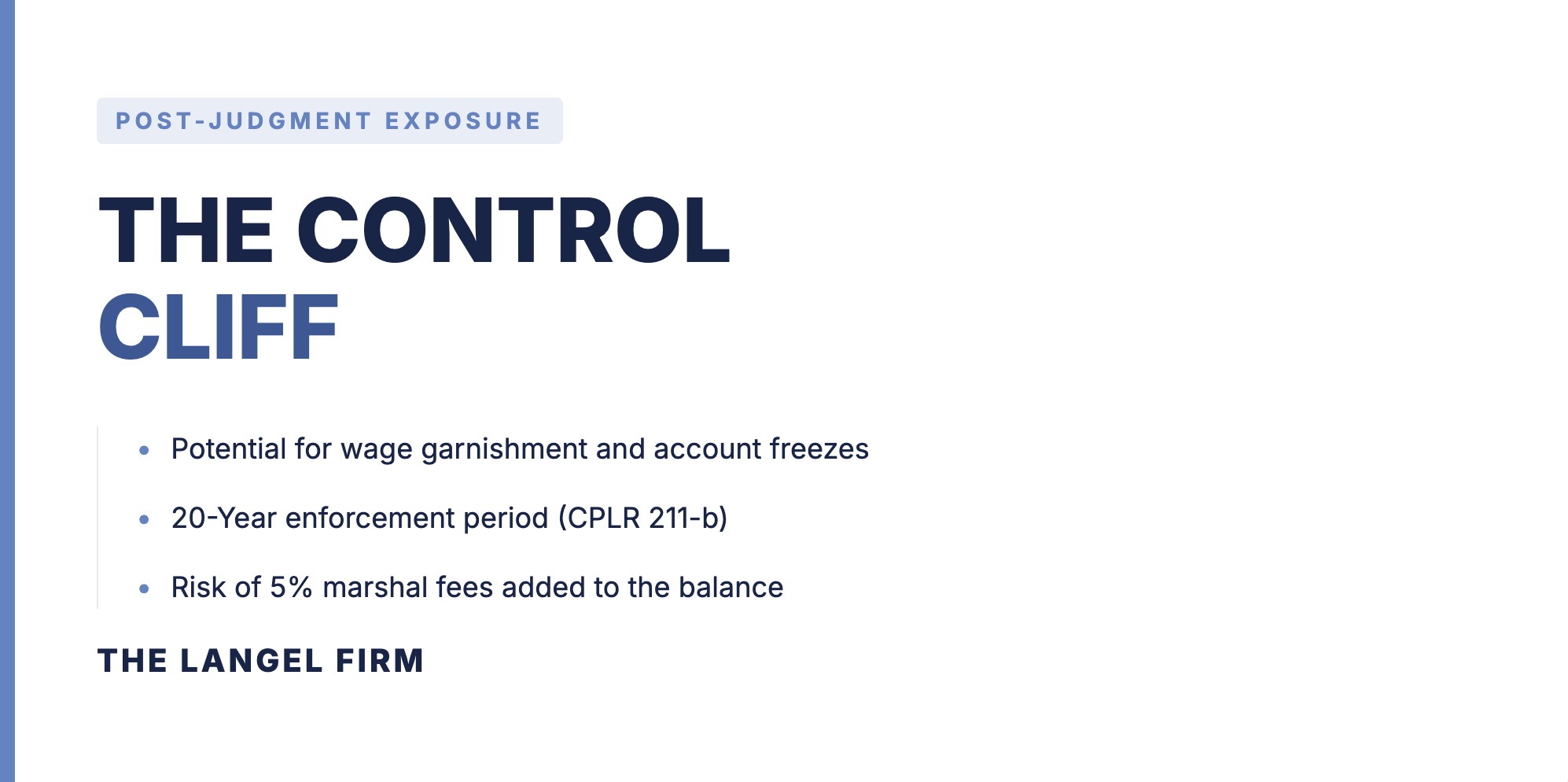

6. What Happens if I Wait Too Long? (The "Control Transfer" Cliff)

Negotiation leverage in NYC is not a slow decline—it is often a cliff. There is a specific moment where the power dynamic shifts significantly toward the creditor.

The "Burn Phase": This is your window. Currently, the creditor is burning resources to maybe collect. This is when they are most motivated to take a settlement.

The "Collection Phase": Once a judgment is entered, settlement options may become more limited and leverage shifts significantly toward the creditor. They can move to garnish wages or freeze bank accounts. At that stage, you are negotiating with fewer defenses and reduced leverage.

7. What is the "Mental Cost" of an Unresolved Lawsuit?

There is an invisible tax on unresolved debt: Cognitive Load. Every morning you wake up with an open lawsuit is a morning you are playing defense.

Buying Back "Mental RAM": Resolving the case reduces the ongoing cognitive and financial burden of active litigation. It allows you to move forward with your career and financial life without a pending legal cloud.

Is "waiting and seeing" a risk? Yes. You don't win by playing chicken with creditors; you win by taking aggressive, informed control.

8. What are the Hidden Penalties of a Judgment?

The "5% Execution Tax": In New York, a statutory enforcement fee (poundage) of up to 5% may be triggered once enforcement is initiated through a marshal or sheriff.

The 20-Year Horizon: A judgment can be enforced for up to 20 years under CPLR 211(b), with liens on real property typically lasting 10 years unless renewed.

The Final Decision: In Practical Terms, Most Cases Follow One of Two Paths:

Take the Offensive: Consider resolving the matter while you still retain the strongest negotiating leverage. Capture the "Triple Stack" of savings and reclaim your peace of mind.

Stay on the Defensive: Wait. Risk the "Control Cliff." Face high contract interest, potential enforcement fees, and a long-term judgment.

Do you want to handle this while you still have control, or wait until the bank does?

Links to Law

The following legal sources and statutes provide the statutory basis for the strategies discussed in this post:

CPLR § 5001: Pre-Judgment Interest – Governs the recovery of interest in contract actions from the date of breach.

CPLR § 5004: 2% Interest Cap – Establishes the 2% rate for money judgments arising out of consumer debt.

CPLR § 3016(j): Pleading Requirements – Mandates specific documentation and itemization for consumer credit lawsuits.

CPLR § 211(b): 20-Year Judgment Life – Sets the twenty-year statute of limitations for the enforcement of a money judgment.

CPLR § 8012: Poundage Fees – Authorizes enforcement fees of up to 5% for marshals and sheriffs.

The Fair Consumer Judgment Interest Act – The 2021 legislation that reduced the consumer judgment rate from 9% to 2%.

General Obligations Law § 5-501: Civil Usury – Defines New York's 16% civil interest cap.

Penal Law § 190.40: Criminal Usury – Sets the 25% criminal interest cap.

Prior results do not guarantee a similar outcome. Contact our office today for a consult at The Langel Firm.