In New York debt collection defense, a recurring pattern frustrates many debtors: a creditor willing to take 20–30% before suit often wants 60–70% or more once a lawsuit is filed or a judgment is entered.

This isn’t just about "more legal fees." It reflects a shift in economics: once a creditor or debt buyer has converted a charged-off account into a judgment, they now hold a stronger, interest-bearing legal claim that can be enforced over time against wages, bank accounts, and property. Consequently, they often price the settlement more aggressively.

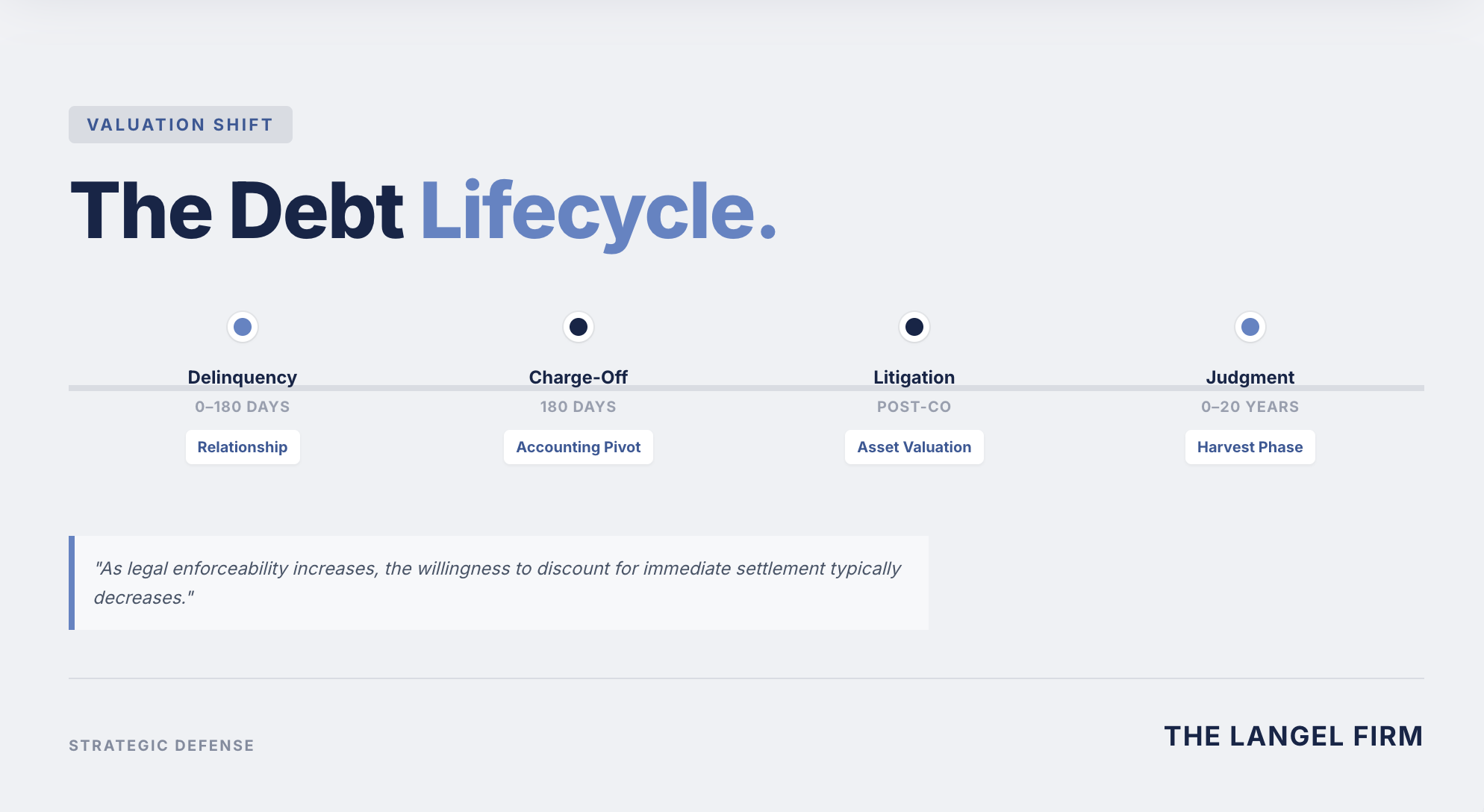

1. The Pre-Charge-Off Phase: The Window for Maximum Flexibility

Before a lawsuit is filed, a bank is typically focused on "loss-mitigation." During this period, their goal is to maximize write-downs and clean up their books for regulatory compliance.

The Preference for Early Resolution Many original creditors prefer early resolution over escalating litigation costs, though practices vary by creditor, account type, and balance size. In practice, some of the steepest discounts may appear before suit, when the account is still being worked as a delinquent receivable rather than as litigated debt. The creditor's primary goal is often to recover a portion of the balance to offset the administrative cost of the default.

Federal Charge-Off Guidance: Under federal interagency retail-credit charge-off guidance (discussed in authorities such as OCC Bulletin 2000-20), open-end credit such as credit-card debt is generally charged off at 180 days delinquent. Once charge-off occurs, the account is generally removed from active receivables and treated as a loss for accounting purposes, even though collection rights remain.

New York Court Rules: New York court rules, specifically 22 NYCRR § 202.27-a, use the concept of "charged-off consumer debt," which is defined as debt removed from an original creditor's books as an asset and treated as a loss or expense.

Accounting Treatment of Recoveries: This accounting treatment may contribute to a shift in incentives, as the account is no longer managed as a customer relationship and is instead evaluated purely for recovery performance. Because the loss was previously recognized, later recoveries may be booked as recoveries on charged-off accounts, which can improve the economics of post-charge-off collection.

2. The Litigation Phase: Why Earlier is Usually Cheaper

Once the account has been charged off for accounting purposes, creditors often reassess whether to litigate, outsource, or sell the account. At this point, the focus often shifts from customer retention to enforcing a legal claim through litigation, assignment, or structured collection efforts.

The Pleading Stage: Contesting the Cost-Model

At the very start of a lawsuit—when you receive the summons and complaint—you still possess significant leverage. The creditor has committed funds to the legal process, but they have not yet secured a victory.

Cost of Litigation vs. Default: For many creditors, an uncontested case is materially cheaper than defended litigation. The creditor’s pricing model often assumes non-participation. When a defendant appears and litigates, the expected value of the claim changes—sometimes significantly—because the cost, delay, and risk assumptions underlying the default model no longer hold.

High Default Rates: Default judgments are common in debt-collection litigation. Various studies report very high rates across jurisdictions, often representing a significant majority of filed cases. Once you answer or move to dismiss, you disrupt the creditor's expectation of a quick, low-cost "win."

Strategic Uncertainty: Before you answer or move under CPLR 3211, the plaintiff may not know whether you will contest ownership of the debt, the chain of assignment, the amount claimed, statute of limitations, or proof of service. They may still accept a lower amount in exchange for certainty and avoiding the cost of active litigation.

If you need help, complete this intake form.

The Shift in Interest Rates: The 2% Factor

CPLR 5004 now provides a 2% annual interest rate in actions arising out of consumer debt where a natural person is the defendant, rather than the usual 9% rate that otherwise applies.

Legislative Intent: The policy behind the amendment was to reduce the burden of high post-judgment interest in consumer-debt cases and to prevent relatively small debts from growing disproportionately over time.

Market Effect: One likely market effect is that a lower statutory interest rate reduces the urgency of immediate collection in some cases, making a longer enforcement timeline more economically acceptable for certain creditors. This lower rate effectively allows institutional players to manage the judgment as a low-yield, low-risk "annuity."

3. Debt Buyer Economics: Long-Term Asset Management

Debt buyers often approach charged-off accounts as purchased receivables whose value depends heavily on collection and litigation performance.

Portfolio Pricing: FTC materials show that many charged-off portfolios are sold for pennies on the dollar. Because portfolios may be purchased at deep discounts, a debt buyer can sometimes realize a strong return even when accepting a settlement well below face value, depending on collection costs and overall portfolio performance.

Collection Modeling: Large debt buyers use portfolio-level collection models (such as "Estimated Remaining Collections" or ERC). As a result, defenses that increase cost, delay, or uncertainty—such as challenging documentation, assignment, or damages—can reduce the expected value of the account within the creditor's model and improve settlement leverage.

The 20-Year Horizon: Under CPLR 211(b), a money judgment is generally enforceable for twenty years, after which it is presumed paid and satisfied. If collection is not feasible immediately, some judgment creditors may wait for later events—such as employment changes or real-estate transactions—that improve collectability.

Preservation of Rights: New York law also allows creditors, through proper procedure, to obtain renewal judgments (CPLR 5014) and to preserve or extend certain lien rights against real property (CPLR 5203). This can make a judgment a long-lived enforcement asset, particularly where the creditor timely preserves its rights.

4. What This Means for Settlement Strategy

To successfully negotiate a debt, you must understand the "pricing logic" of the entity holding the claim:

Early Delinquency: Leverage is high because the creditor is pricing uncertainty (will they pay at all?) and trying to avoid the 180-day charge-off loss.

Post-Filing: Leverage depends on disruption. The creditor’s model expects a default; when you appear and contest the chain of title or service, you force them to re-evaluate the cost of the "harvest."

Post-Judgment: Leverage is driven by reachability. If a creditor believes your assets are exempt or that enforcement will be too costly over a 20-year span, they may still accept a lump sum to close the file.

Summary

The transition from a 30% offer to a 70% demand is rarely arbitrary; it is the result of a debt moving from a "Relationship" model to a "Judgment Asset" model. In practical terms, the debt has shifted from a relationship problem to an asset problem: once reduced to judgment, the account is no longer negotiated as a customer balance, but managed as an enforceable financial instrument.

Links to Law

New York Statutes & Court Rules

- CPLR § 5004 – Interest Rate on Judgments (2% for Consumer Debt Cases)

https://www.nysenate.gov/legislation/laws/CVP/5004 - CPLR § 211(b) – Twenty-Year Enforcement of Money Judgments

https://www.nysenate.gov/legislation/laws/CVP/211 - CPLR § 5014 – Action Upon a Judgment (Renewal Judgments)

https://www.nysenate.gov/legislation/laws/CVP/5014 - CPLR § 5203 – Judgment Liens on Real Property

https://www.nysenate.gov/legislation/laws/CVP/5203 - CPLR Article 52 – Enforcement of Money Judgments (Overview)

https://www.nysenate.gov/legislation/laws/CVP/A52 - 22 NYCRR § 202.27-a – Consumer Credit Default Judgments and Charged-Off Debt

https://ww2.nycourts.gov/rules/trialcourts/202.shtml - CPLR § 3215 – Default Judgments

https://www.nysenate.gov/legislation/laws/CVP/3215

Federal & Industry Context

- OCC Bulletin 2000-20 – Charge-Off Guidance

https://www.occ.treas.gov/news-issuances/bulletins/2000/bulletin-2000-20.html - FTC – Debt Buying Industry Report

https://www.ftc.gov/system/files/documents/reports/structure-and-practices-debt-buying-industry/debtbuyingreport.pdf - Pew – Debt Collection Lawsuits & Default Trends

https://www.pewtrusts.org/en/research-and-analysis/reports/2020/05/how-debt-collectors-are-transforming-the-business-of-state-courts

Educational analysis only. Not individualized legal advice.