The Homestead Exemption law in New York, as detailed in § 5206, safeguards a person's primary residence from being used to satisfy a monetary judgment. The government's policy in implementing the homestead exemption in CPLR § 5206 is to protect from seizure the reasonable living requirements of the debtor and his or her family. All exemptions are considered "privileges" expressly provided by law. If you need help, complete this intake form.![]()

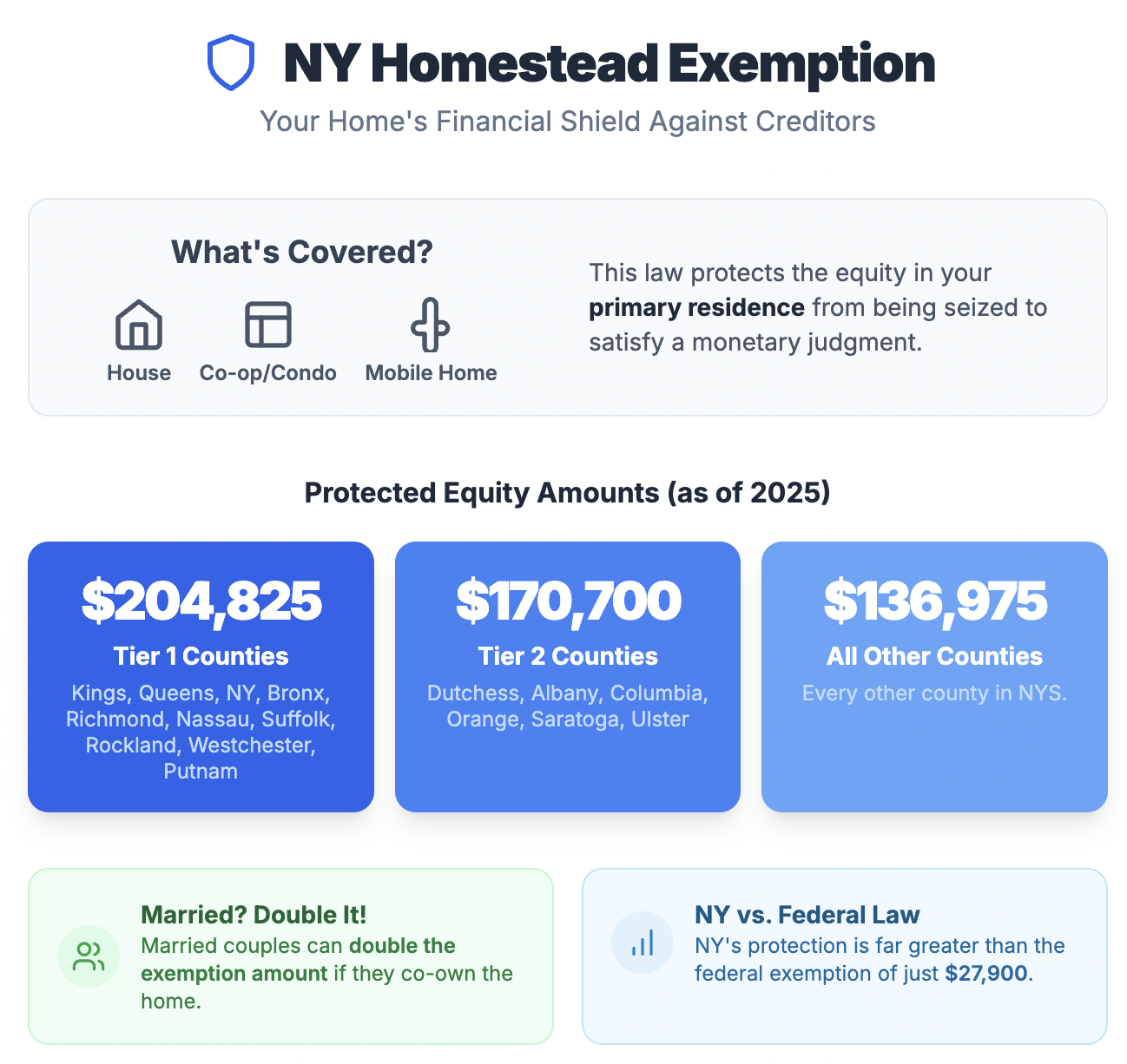

What is a "Homestead?"

Basically, it's your home that you physically occupy as a principal residence. A vacation or weekend home will not qualify. A homestead can be one of the following:

- House;

- Shares in a coop;

- Unit(s) of a condo; or

- A mobile home.

What is a "Homestead Exemption"?

It's the amount of equity in your home above "liens and encumbrances." The amounts invested in the home below are protected from seizure.

How much money equity in the home is protected by the homestead exemption (As of 2025)?

- $204,825 for the following counties: Kings (Brooklyn), Queens, New York, Bronx, Richmond, Nassau, Suffolk, Rockland, Westchester, and Putnam.

- $170,700 for the following counties: Dutchess, Albany, Columbia, Orange, Saratoga, and Ulster.

- $136,975 for any other county.

If your equity amount exceeds the exemption, the judgment creditor can force a sale of your home and apply that surplus to the judgment. The sale is subject to court discretion.

The exemption allowed in Federal Bankruptcy Court is only $$27,900—a fraction of what New York allows. Thus, electing New York exemptions in a bankruptcy petition provides a stark advantage. This amount is scheduled The next adjustment is scheduled for April 1, 2027.

New York permits married couples to double the homestead exemption. For a married couple in New York County (a high-cost county), the total exemption would be $409,650 ($204,825 x 2) for New York County.

After a forced sale of the homestead, the exempt money paid to the judgment debtor is exempt for one year after payment unless that money is used to acquire another exempt homestead.

The homestead exemption continues after the death of the judgment debtor for the benefit of the surviving spouse and surviving children until the youngest child reaches majority age and the surviving spouse is dead. The same rationale applies to protecting exemption amounts in personal property, as addressed in our previous blog.

How Debt Collectors Can Place Liens on Homes in New York

In New York, creditors who have obtained money judgments for unpaid debts can create liens against a debtor's real property by docketing the judgment with the county clerk where the property is located. This process involves filing a Transcript of Judgment, which creates a lien that remains effective for ten years and can be renewed up to two times. The lien secures the creditor's priority and allows them to foreclose on the property if the debtor fails to pay the debt.

- Docketing a judgment with the county clerk creates a lien on the debtor's real property in that county

- The lien remains effective for ten years and can be renewed twice, provided the creditor follows the proper procedures outlined in CPLR 5014.

- For more about the Lien Docketing Process, see Can a Debt Collector Place a Lien on my Home? Yes, Here's How

The Rationale and Limits of New York's Homestead Exemption

When a creditor obtains a court judgment on a debt, even for just a credit card or medical debt, the creditor can then put a lien on your home for the amount of the judgment. With a lien in place, the creditor can then force a sale of your home to recover its judgment amount. Alternatively, the creditor can simply hold on to its lien and wait for you to sell the home before seeking to collect on the lien.

Keep in mind that the homestead exemption does not apply to 1) mortgage foreclosure actions (first or second mortgages); 2) home equity lines of credit; 3) actions where your home as collateral for a different debt; or 4) forced sales for the non-payment of tax debt.

How to Determine Your Home Equity and Eligibility for the Homestead Exemption

We'll walk you through the steps to calculate your home equity and determine whether you qualify for the exemption.

Calculating Your Home Equity: Home equity is the difference between your home's current market value and the outstanding balance on your mortgage and any other liens on the property. To calculate your home equity:

- Determine your home's current market value. You can use online tools, consult a real estate agent, or hire a professional appraiser.

- Add up the balances of your mortgage and any other liens on the property, such as home equity loans or lines of credit.

- Subtract the total liens from your home's current market value. The result is your home equity.

For example, if your home is worth $500,000 and you have a mortgage balance of $300,000, your home equity is $200,000.

Eligibility for the Homestead Exemption: To be eligible for the Homestead Exemption in New York, you must meet the following criteria:

- The property must be your primary residence. Vacation homes, investment properties, and second homes do not qualify.

- You must own the property and have an equity interest in it. This includes houses, condominiums, co-ops, and mobile homes.

- Your home equity must fall within the exemption limits for your county:

- $204,825 for the counties of Kings, Queens, New York, Bronx, Richmond, Nassau, Suffolk, Rockland, Westchester, and Putnam.

- $170,700 for the counties of Dutchess, Albany, Columbia, Orange, Saratoga, and Ulster.

- $136,975 for all other counties.

If your home equity exceeds the exemption limit, creditors may be able to force the sale of your home to satisfy a judgment. However, you will still be entitled to the exempt amount from the sale proceeds.

Special Considerations:

- Married couples can double the exemption amount if they both own the property and reside there as their primary residence.

- The Homestead Exemption does not protect against mortgage foreclosure, property tax liens, or judgments related to the purchase or improvement of the property.

- If you file for bankruptcy in 2024, you may choose between the New York State Homestead Exemption or the federal exemption, but you cannot mix exemptions from both schemes. The federal homestead exemption offers a lower level of protection ($27,900 as of 2024) compared to New York's exemption.

Advantages of New York's Homestead Exemption Over Federal Bankruptcy Law

When it comes to protecting your primary residence from creditors, New York State's Homestead Exemption offers several advantages over the federal exemption available in bankruptcy proceedings.

Higher Exemption Amounts: One of the most significant advantages of New York's Homestead Exemption is the substantially higher exemption amounts compared to the federal bankruptcy exemption. As of 2024, the federal homestead exemption is $27,900 for an individual and $55,800 for married couples filing jointly. In contrast, New York's exemption amounts are:

- $204,825 for the counties of Kings, Queens, New York, Bronx, Richmond, Nassau, Suffolk, Rockland, Westchester, and Putnam.

- $170,700 for the counties of Dutchess, Albany, Columbia, Orange, Saratoga, and Ulster.

- $136,975 for all other counties.

These higher exemption amounts provide greater protection for your home equity, especially in counties with higher property values.

- No Residency Requirement: To claim the federal homestead exemption in bankruptcy, you must have lived in the state where you're filing for at least 40 months (about 3.5 years) before the bankruptcy petition. If you haven't met this residency requirement, you may be limited to the exemption amount allowed by your previous state of residence.

- New York's Homestead Exemption does not have a residency requirement. As long as the property is your primary residence at the time you claim the exemption, you can take advantage of the state's protection.

- Doubling the Exemption for Married Couples: Under New York law, married couples can double the Homestead Exemption amount if they both own the property and use it as their primary residence. For example, married couples in New York County can protect up to $300,000 of their home equity.

Conversely, the federal exemption only allows married couples filing jointly to claim $50,300, which may not provide sufficient protection in areas with high property values.

Avoiding the Complexity of Bankruptcy: By relying on New York's Homestead Exemption, you may be able to protect your primary residence from creditors without the need to file for bankruptcy. Bankruptcy proceedings can be complex, time-consuming, and may have long-lasting consequences on your credit score and financial future.

Using the state exemption law allows you to safeguard your home equity while exploring alternative debt relief options, such as negotiating with creditors or seeking legal guidance on debt management strategies.

Can a judgment lien in NY lead to foreclosure if unpaid for 10 years?

While the federal bankruptcy exemption provides a baseline level of protection for your primary residence, New York State's Homestead Exemption offers significantly higher exemption amounts, no residency requirement, and the ability for married couples to double their protection.

A judgment lien in New York can potentially lead to foreclosure if it remains unpaid, but the timing and process are specific:

Judgment liens last for 10 years from the date they are docketed with the county clerk. Before the 10-year period expires, the creditor can renew the lien for another 10 years by following the proper legal procedures.

A judgment itself is enforceable for 20 years in New York, even if the lien on real property is only valid for 10 years at a time and must be renewed to maintain its effect on the property.

Foreclosure is possible: If the debtor's home equity exceeds any applicable exemptions (such as the homestead exemption), a judgment creditor can seek a court order to force the sale of the property to satisfy the debt. This action can be taken at any time while the judgment lien is valid and effective, not just after 10 years. If the lien is not renewed after 10 years, it lapses and the creditor loses their secured interest in the property.

Three Core Takeaways from the Homestead Exemption in New York

- Principal Residence Required: The Homestead Exemption in New York only applies to the debtor's primary residence. Secondary properties or vacation homes are not protected under this law. The homeowner needs to live in the property on a regular basis for it to qualify.

- Co-ops and Condos Included, but Caution on Liens: The exemption extends to co-op and condo apartments. However, these property types may not be considered real estate when determining judgment liens and priorities. Particularly, shares in a cooperative apartment are considered personal property for this purpose.

- Limited Exemption for Mortgages and Foreclosures: The exemption does not prevent a mortgage lender from seizing the property in case of loan default. It also doesn't apply to proceeds from the foreclosure sale. The exemption is also lifted once the debtor ceases to inhabit the property, even if it was their primary residence before. This also includes cases where a surplus results after the sale in foreclosure, which is considered personal property and not covered by the exemption.

The Purpose of New York's Homestead Exemption: Insights from Case Law

- The homestead exemption aims to shield a homeowner's dwelling from seizure to fulfill a money judgment. This protection serves in both non-bankruptcy and bankruptcy scenarios (CFCU Community Credit Union v. Hayward, C.A.2 (N.Y.) 2009, 552 F.3d 253, In re Flatt, 1993, 160 B.R. 497).

- It safeguards the debtor-homeowner from losing their family residence due to economic hardship (In re Issa, 2013, 501 B.R. 223).

- The exemption traditionally seeks to protect the family of a judgment debtor by exempting their home from execution on an outstanding money judgment (Michaels v. Chemical Bank, 1981, 110 Misc.2d 74, 441 N.Y.S.2d 638).

- The homestead exemption is designed to offer homeowners certain protection against creditors, barring those with a purchase mortgage to which the exemption doesn't apply (Wyoming County Bank & Trust Co. v. Kiley (4 Dept. 1980) 75 A.D.2d 477, 430 N.Y.S.2d 900).

- Amendments to the exemption, such as an increase from $10,000 to $50,000, reflect a legislative intent to adjust for inflation and align the exemption with current economic conditions, offering a realistic safeguard in today's economy (CFCU Community Credit Union v. Hayward, C.A.2 (N.Y.)2009, 552 F.3d 253).

- These amendments are intended to apply to all debtors who file for bankruptcy after the amendment's effective date, irrespective of when the debt was incurred or reduced to a judgment (1256 Hertel Ave. Associates, LLC v. Calloway, C.A.2 (N.Y.)2014, 761 F.3d 252).

![]()

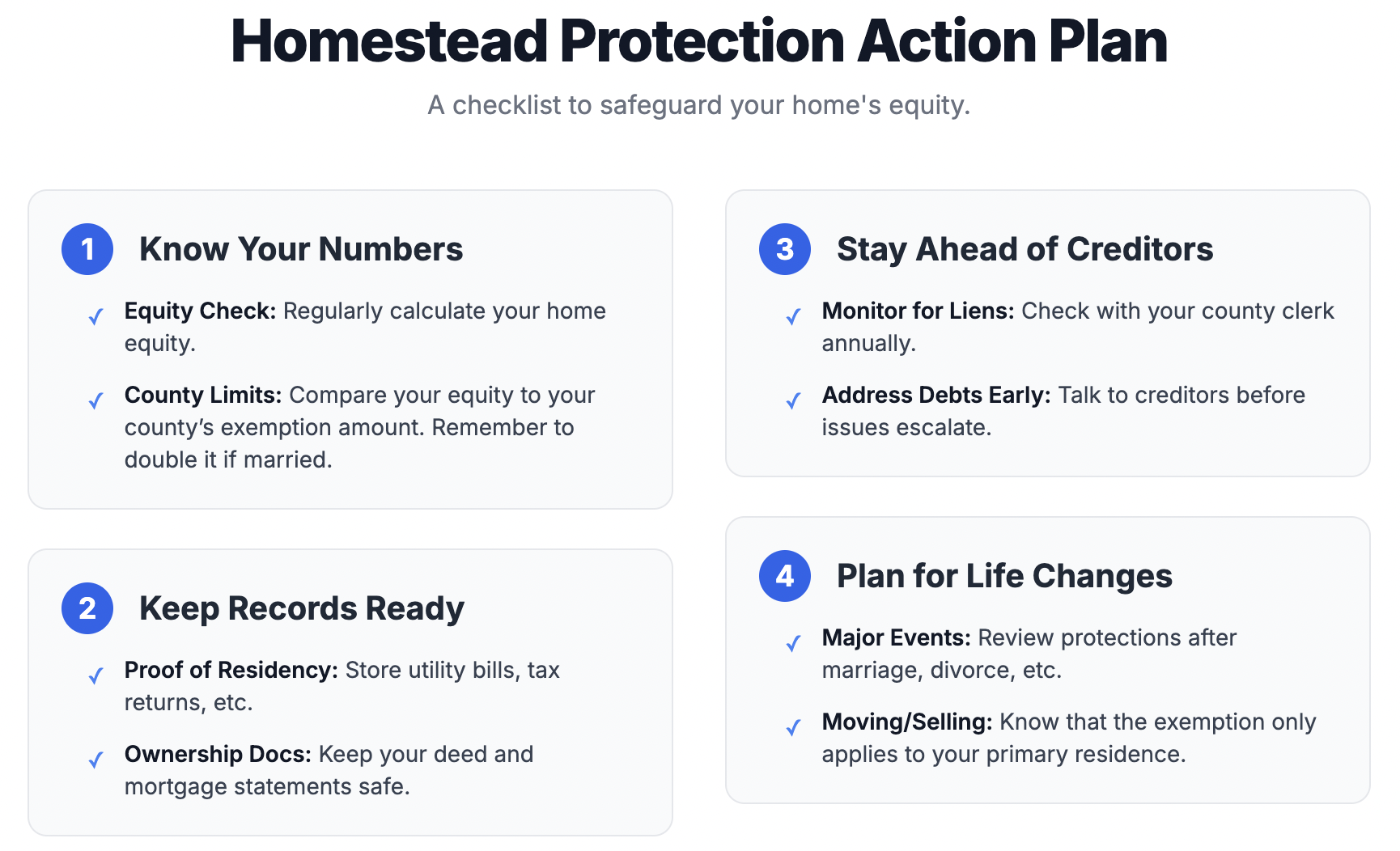

Your Personalized Protection Checklist

1. Know Your Numbers:

Equity Check: Regularly calculate your home equity. Use online estimators, or consult a real estate agent for a more precise valuation.

County Limits: Find your county’s exemption amount and compare it to your equity. If you’re married and both own the home, remember—you can double the protection.

2. Keep Your Records Ready:

Proof of Residency: Store utility bills, tax returns, and voter registration showing you live at your home.

Ownership Documents: Keep your deed, mortgage statements, and any co-op or condo share certificates in a safe place.

3. Stay Ahead of Creditors:

Monitor for Liens: Check with your county clerk’s office once a year to see if any liens have been filed against your property.

Address Debts Early: If you’re struggling with debt, talk to creditors or a financial counselor before things escalate.

4. Plan for Life Changes:

Marriage, Divorce, or Inheritance: Major life events can affect your exemption. Review your protections whenever your household changes.

Moving or Selling: If you plan to move, know that your exemption only applies to your primary residence.

Beyond the Basics: Creative Strategies

Refinance Wisely: If your equity is well above the exemption, consider refinancing to pay down high-interest debts, reducing the risk of losing non-exempt equity.

Homestead Proceeds: If your home is sold to satisfy a judgment, the exempt proceeds are protected for one year. Use this time to reinvest in another qualifying homestead if possible.

Community Resources: Many New York nonprofits and legal aid organizations offer free or low-cost consultations. Don’t hesitate to reach out—they’re there to help.

The Langel Firm seeks to keep you out of bankruptcy and out of hairy situations involving judgment liens over credit card debt. We primarily handle cases brought by unsecured creditors such in ourl debt collector list). These creditors may obtain money judgments that eventually turn into liens against your home (see this blog post to see how it's done), but I have yet to see one of these unsecured creditors attempt a forced sale of your home to satisfy such a money judgment. That is partly because of the exemption provided by CPLR § 5206.

In conclusion, the Homestead Exemption law under § 5206 in New York State protects a debtor's primary residence from becoming collateral against monetary judgments. However, it's crucial to understand its parameters - it's not a catch-all solution. The exemption does not apply to foreclosures nor cases where your home has been pledged as collateral for other debts. Furthermore, the law only protects primary residences, not vacation homes or secondary properties.