In New York debt collection, many judgment debtors are surprised to find their bank accounts frozen and funds nearly seized by a City Marshal or Sheriff before any restraining notice is served—whether by the judgment creditor or through enforcement channels. This "levy-first" approach is often used by high-volume collection firms to accelerate enforcement rather than proceeding through intermediate steps such as restraining notices or additional investigation.

While this approach is collection-efficient, it often creates legal and procedural complications when the target is a joint account or an account located outside New York. Understanding why this happens—and why a freeze remains even if the bank refuses to turn over the money—is critical for protecting your assets and those of your co-owners.

Why Did a Marshal Levy My Account Instead of the Lawyer Just Sending a Restraining Notice?

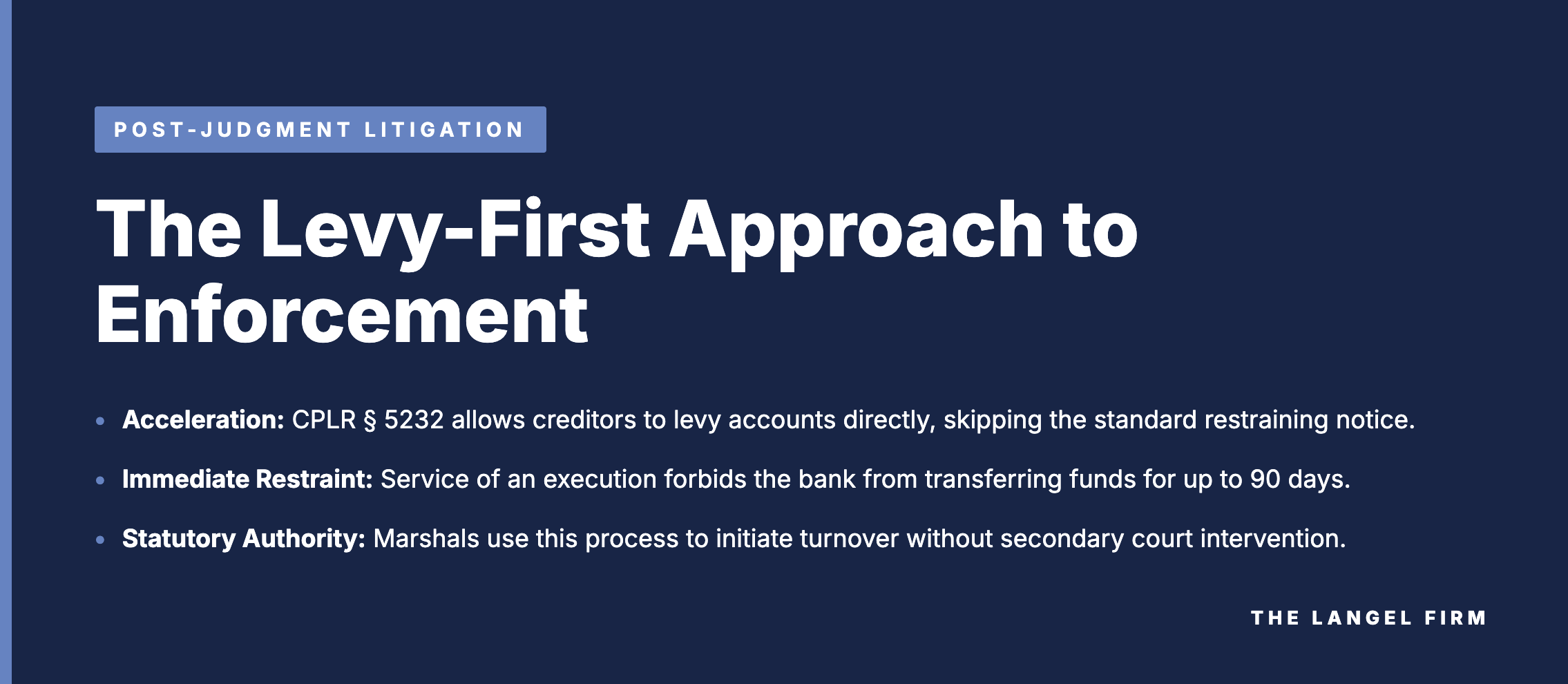

Under New York law, a creditor does not have to follow a specific sequence. They are not required to "start" with a restraining notice before using a more aggressive tool. There are two primary reasons why institutional creditors default to a bank levy (execution):

Acceleration of the Payment Pipeline: Under CPLR § 5232, when a Marshal serves an execution on a bank, it both restrains the account and initiates the process by which the garnishee may be required to turn over funds, subject to statutory protections and competing claims.

CPLR § 5232(a) provides: "The officer shall levy upon any interest of the judgment debtor in personal property... by serving a copy of the execution upon the garnishee... A levy by service of the execution is effective only if, at the time of service, the person served owes a debt to the judgment debtor or is in the possession or custody of property not capable of delivery in which he knows or has reason to believe the judgment debtor has an interest."

The bank may remit funds after the applicable Exempt Income Protection Act (EIPA) waiting period if no exemption claim or legal impediment exists; however, payment is not automatic and may be delayed by disputes, exemptions, or internal review. A restraining notice under CPLR § 5222 merely "preserves the pot" but does not move any money without a later levy or turnover order.

Streamlining the Enforcement Path: While a standard restraining notice under CPLR § 5222 freezes the account the moment it is served, it requires the creditor to take a second enforcement step—issuing an execution or starting a turnover proceeding—to reach the funds. By proceeding directly to a levy, the creditor uses a more streamlined process that can lead to payment without requiring a separate enforcement step, subject to statutory and practical constraints.

CPLR § 5222(b) states: "A judgment debtor or obligor served with a restraining notice is forbidden to make or suffer any sale, assignment, transfer or interference with any property in which he or she has an interest... except upon direction of the sheriff or pursuant to an order of the court, until the judgment or order is satisfied or vacated."

Why Does the Bank Levy Often Stall When the Creditor Targets a Joint Bank Account?

The "levy-first" strategy often meets resistance when it hits a joint account. In this scenario, the creditor’s path to payment is frequently blocked by two major hurdles:

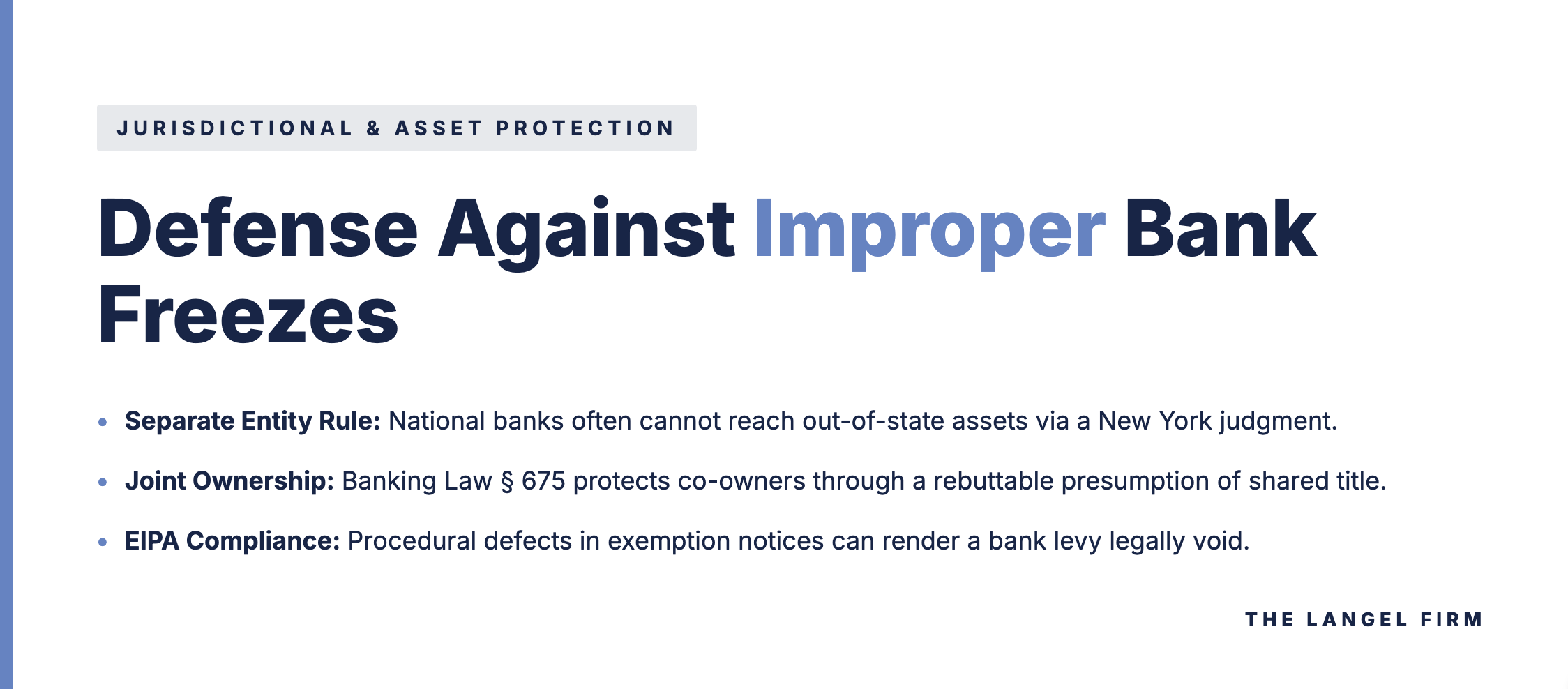

The Presumption of Joint Ownership: In New York, the ownership of a joint account is governed by Banking Law § 675. This statute creates a prima facie presumption of joint ownership (joint tenancy with survivorship), though the actual beneficial ownership may differ based on the parties’ contributions and intent.

Banking Law § 675(b) provides: "The making of such deposit... shall, in the absence of fraud or undue influence, be prima facie evidence... of the intention of both depositors or shareholders to create a joint tenancy and to vest title to such deposit... in such survivor."

As discussed in Piccarreto v. Mura, 51 Misc. 3d 1230(A) (Sup. Ct. Monroe Co. 2016), creditors must navigate "reasonable requirements" and ownership disputes because of this shared ownership. Banks frequently decline to remit funds beyond the debtor’s presumptive share absent a court order, due to potential liability to the non-debtor co-owner.

EIPA Procedural Defects: For natural persons, noncompliance with EIPA notice requirements may render the restraint or levy defective and subject to vacatur. On joint accounts, the risk of hitting exempt funds belonging to a co-owner is significantly higher, leading banks to demand judicial clarification before honoring the levy.

Can a Creditor Reach More Than the Debtor's Presumptive Share?

While Banking Law § 675 presumes joint ownership, that presumption is rebuttable. In Ford Motor Credit Co. v. Astoria Federal, 189 Misc. 2d 575 (Dist. Ct. Nassau Co. 2001), the court held that when a non-debtor co-tenant is personally served with a turnover petition and fails to answer, that default may permit the court to deem the petition’s allegations admitted, potentially overcoming the ownership presumption if sufficiently supported. This can result in a court authorizing turnover of more than the debtor’s presumptive share, potentially up to the full balance.

Why Did Chase Freeze My Out-of-State Bank Account for a New York Judgment?

When a New York creditor serves a levy or restraining notice on a national bank—even through its New York registered agent—jurisdictional conflicts arise if the account is located elsewhere. This triggers the Separate Entity Rule, a doctrine reaffirmed in Motorola Credit Corp. v. Standard Chartered Bank, 24 N.Y.3d 149 (2014) and Limonium Maritime S.A. v. Mizuho Corporate Bank, 961 F. Supp. 600 (S.D.N.Y. 1997).

The Separate Entity Rule treats each bank branch, and often each state-situs account, as a separate legal entity for enforcement purposes. Simply serving a bank’s New York headquarters does not automatically grant a New York Marshal the authority to seize an account maintained in another jurisdiction.

In these cases, some banks impose internal review periods—often extending beyond statutory minimums—where jurisdictional or compliance issues arise. This "safety window" serves two purposes:

Liability Protection: The bank is caught between a New York order and the consumer protection laws of the debtor’s home state. Turning over the money prematurely exposes the bank to liability if home-state wage or account exemptions are violated.

Jurisdictional Review: The bank may release or modify the restraint if no enforceable basis for turnover—such as a domesticated home-state judgment—is established within its review period.

Can I Accelerate the Review of an Improper Bank Freeze?

In practice, what is often described as "escalation" refers to internal review by a bank’s legal or levy-processing unit, which may reassess the restraint in light of jurisdictional or exemption issues.

Because many national banks centralize legal process handling, direct contact with the designated legal processing unit (often via specialized branch-level requests) may facilitate substantive review. Escalation is most effective when the debtor can present immediate evidence that flips the bank's liability risk:

Proof the account is truly out of state: Valid home-state identification, utility bills, or lease agreements showing a lack of New York ties.

Proof of exempt status: Direct deposit records or paystubs showing that the funds are wages protected under the debtor’s home-state law and the EIPA framework under CPLR § 5222-a.

Once these materials are presented to a higher-tier review group, the bank has a stronger incentive to lift or narrow the restraint rather than risk a lawsuit for violating home-state consumer protections.

If the Bank Declined to Pay the Marshal, Why Is My Account Still Frozen?

This common frustration occurs because service of the execution creates a statutory restraint that functions as an injunction against transfer of the property. Under CPLR § 5232(a), the service of the "Execution with Notice to Garnishee" explicitly forbids the bank from transferring or disposing of the funds. This restraint generally remains effective for up to ninety days from service, subject to extension or further court proceedings.

The bank essentially acts as a "neutral stakeholder," maintaining the status quo to protect itself from liability while the legal ownership or jurisdictional validity of the funds is resolved.

Strategic Leverage: Challenging the "Self-Help" Bank Freeze

While creditors may proceed directly to execution, doing so can introduce legal complexities that may be challenged by debtors or co-owners:

Formal Legal Review: Challenging the jurisdiction of a New York levy on an out-of-state account via the bank's centralized legal orders unit.

Banking Law § 675 Burden: Forcing the creditor to provide affirmative evidence of beneficial ownership beyond the joint tenancy presumption.

Mutuality Defenses: As established in Matter of Sanger, 2014 N.Y. Slip Op. 24371 (Sur. Ct. Nassau Co. 2014), challenging bank sweeps that lack mutual indebtedness (e.g., personal vs. corporate accounts).

CPLR § 5240 Protective Orders: Invoking the court's power to deny, limit, or modify enforcement procedures to prevent abuse or hardship.

At The Langel Firm, we emphasize that a rigorous procedural defense is often the most effective way to protect liquidity when facing aggressive enforcement.

Links to Law

New York Statutes (CPLR & Banking Law)

CPLR § 5232: Levy Upon Personal Property The primary statute governing how Marshals and Sheriffs "freeze" bank accounts through service of an execution.

CPLR § 5222: Restraining Notice The legal authority for the injunctive "freeze" that prevents a debtor or bank from moving assets.

CPLR § 5222-a: Service of Notice and Exemption Claim Forms The procedural heart of the Exempt Income Protection Act (EIPA), which protects certain funds from collection.

Banking Law § 675: Joint Deposits and Shares; Ownership and Payment The statute that establishes the prima facie presumption of joint tenancy (shared ownership) in bank accounts.

CPLR § 5225: Payment or Delivery of Property (Turnover Proceeding) The specialized proceeding used to resolve ownership disputes when property is held by a third party like a bank.

CPLR § 5240: Modification or Protective Order The "safety valve" that allows New York courts to deny, limit, or regulate any enforcement procedure to prevent abuse.

Significant New York Case Law

Piccarreto v. Mura, 51 Misc. 3d 1230(A) (Sup. Ct. Monroe Co. 2016) A case illustrating the complexities of "reasonable requirements" and ownership disputes in the context of joint marital property.

Matter of Sanger, 2014 N.Y. Slip Op. 24371 (Sur. Ct. Nassau Co. 2014) The foundational case for the "lack of mutuality" defense against bank sweeps (e.g., trying to offset a corporate debt with personal funds).

Motorola Credit Corp. v. Standard Chartered Bank (24 N.Y.3d 149): This is the "gold standard" Court of Appeals case for the Separate Entity Rule. It explicitly holds that the rule survives the Koehler decision and protects foreign branches from New York restraining notices.

Ford Motor Credit Co. v. Astoria Federal (189 Misc. 2d 575): This is a key "warning" case. It confirms that in a turnover proceeding, the failure of a non-debtor co-owner to appear (default) can be used by a court to find that the joint tenancy presumption has been rebutted.

Educational analysis only. Not individualized legal advice.