Applying Debt Defense Expertise to Commercial Guarantor Advisory

I've built The Langel Firm around collection defense and post-judgment enforcement protection in New York. Over fifteen years, I've developed expertise in CPLR Article 52, exemption law, and the procedural mechanisms creditors use to enforce judgments. That technical knowledge now informs a growing part of my practice: strategic advisory for guarantors facing personal liability on commercial lease obligations.

The challenge guarantors face is straightforward: they signed agreements during favorable business conditions, often without fully understanding enforcement implications. When the business struggles or fails, the guaranty becomes the landlord's primary collection vehicle—and most guarantors don't realize the exposure until enforcement has already begun.

The Enforcement Perspective

My background differs from traditional real estate counsel. I focus on what happens after default: how landlords enforce guaranties, what procedural tools they use, and which legal protections limit their reach.

This includes exemption law application (understanding which income and assets New York law protects from restraining notices and garnishments), procedural defense (identifying defects in service and notice requirements), and asset protection strategy (analyzing ownership structures and statutory exemptions to determine realistic exposure).

If you need help, complete this intake form.

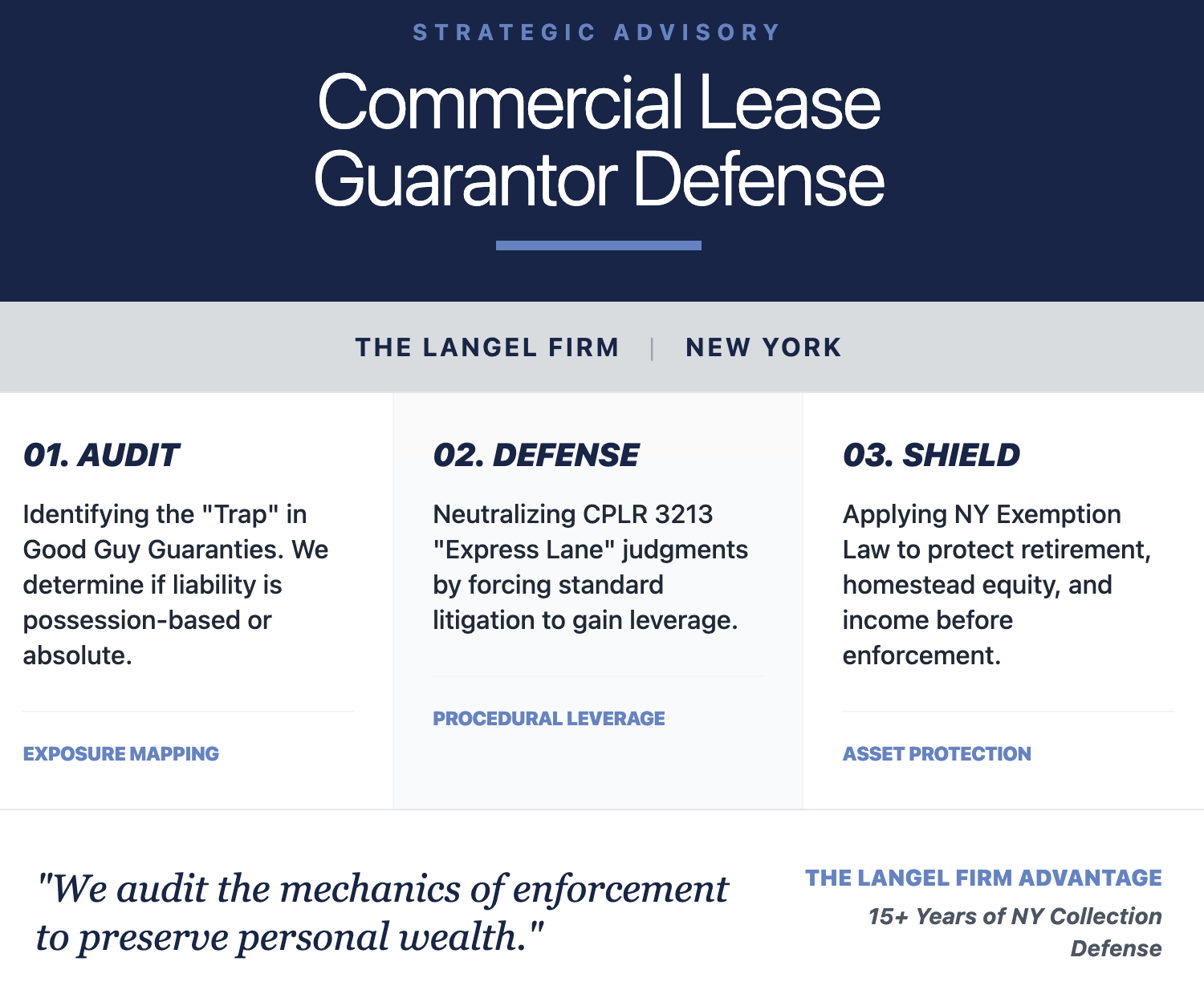

The "Lease Liability Audit"

I provide consultations to evaluate guarantor exposure before landlords initiate enforcement. This analysis examines guaranty language, lease terms, and procedural compliance to identify limitations on personal liability.

The Critical Distinction: "Good Guy" vs. Absolute Guaranties

The first question is whether you signed a "Good Guy Guaranty" (GGG) or an Absolute Guaranty. This distinction determines whether you can terminate liability by vacating and surrendering possession.

Under New York case law, a properly structured Good Guy Guaranty allows the guarantor to cut off liability by vacating the premises and surrendering the keys—even if the landlord refuses to accept them—provided the guaranty does not explicitly require written landlord acceptance.

The Trap: Incorporated Lease Terms

The analysis becomes complex when the guaranty incorporates the lease's surrender requirements by reference. If the guaranty explicitly adopts lease provisions requiring landlord consent or written acceptance, the guarantor cannot unilaterally terminate liability by simple vacation.

We review guaranty language to determine whether it stands alone or incorporates lease surrender terms, whether landlord acceptance is required, whether notice requirements have been satisfied, and whether the guarantor has complied with all conditions precedent to termination.

Defending CPLR 3213 Motions

Landlords frequently use CPLR 3213 summary proceedings to obtain fast judgments on guaranties. This "express lane" procedure allows judgment based on documentary evidence alone—but only when the guaranty qualifies as an "instrument for the payment of money only."

Protecting Personal Wealth: Strategic Advisory for Commercial Lease Guarantors

I built The Langel Firm around collection defense and post-judgment enforcement protection in New York. For more than fifteen years, my practice has focused on how creditors actually enforce judgments—particularly under CPLR Article 52 and New York exemption law. That enforcement-side experience now informs a core part of my practice: strategic advisory for individuals who have personally guaranteed commercial leases.

Guaranties are often signed when businesses are healthy and leverage feels remote. When operations falter, however, the guaranty becomes the landlord’s primary collection tool—and many guarantors do not understand the scope of their personal exposure until enforcement is already underway.

The Enforcement Perspective

My background differs from traditional real estate counsel. I focus on what happens after default: how landlords enforce guaranties, what procedural tools they use, and which legal protections limit their reach.

Pre-Default Advisory: The "Lease Liability Audit"

I provide strategic consultations to evaluate guarantor exposure before landlords initiate enforcement. This analysis examines guaranty language, lease terms, and procedural compliance to identify limitations on personal liability.

Key analysis areas include:

Exposure mapping: Determining if liability is "possession-based" (ends when tenant vacates) or "default-based" (triggering full liability immediately upon nonpayment)

"Good Guy" classification: Assessing whether the guaranty stands alone or incorporates lease surrender requirements by reference

Portfolio risk assessment: For clients with multiple locations, analyzing "cross-default" clauses to determine if closing one failing location triggers personal liability across the entire portfolio

Modification review: Checking if the lease was modified (rent deferred, term extended) without the guarantor's signature, which may discharge the guarantor under New York case law unless the guaranty contains specific "advance consent" waivers

The Critical Distinction: "Good Guy" vs. Absolute Guaranties

The first question is whether you signed a "Good Guy Guaranty" (GGG) or an Absolute Guaranty. This distinction determines whether you can terminate liability by vacating and surrendering possession.

Under New York case law, a properly structured Good Guy Guaranty allows the guarantor to cut off liability by vacating the premises and surrendering the keys—even if the landlord refuses to accept them—provided the guaranty does not explicitly require written landlord acceptance. Recent appellate decisions have clarified that physical surrender can terminate liability when the guaranty stands independent of lease surrender provisions.

The Trap: Incorporated Lease Terms

The analysis becomes complex when the guaranty incorporates the lease's surrender requirements by reference. If the guaranty explicitly adopts lease provisions requiring landlord consent or written acceptance, the guarantor cannot unilaterally terminate liability by simple vacation.

We review guaranty language to determine:

Whether it stands alone or incorporates lease surrender terms

Whether landlord acceptance is required or surrender is self-executing

Whether notice requirements specify timing (30, 60, or 90 days) and delivery method

Whether the guarantor has complied with all conditions precedent to termination

Whether "step-in rights" exist that allow the guarantor to force surrender when the tenant entity is uncooperative

The Surrender Execution Strategy

For guarantors planning exit from struggling businesses, we manage the tenant's departure to ensure liability termination. This includes documenting physical condition to "broom clean" standards with video and photographs, drafting and serving surrender notices exactly as required by guaranty terms, and asserting unilateral surrender rights when landlords refuse to sign formal agreements.

Proper execution of surrender protocols prevents landlords from later claiming extended liability periods that inflate damages—a common dispute when guarantors simply walk away without following precise contractual procedures.

Defending CPLR 3213 Motions

Landlords frequently use CPLR 3213 summary proceedings to obtain fast judgments on guaranties. This "express lane" procedure allows judgment based on documentary evidence alone—but only when the guaranty qualifies as an "instrument for the payment of money only."

We evaluate whether the guaranty requires outside proof that disqualifies it from CPLR 3213:

Does enforcement depend on proving the tenant failed to perform non-monetary obligations (maintenance, insurance, permit delivery)?

Must the landlord demonstrate compliance with notice and cure requirements?

Are there disputed factual issues about whether conditions precedent were satisfied?

Does the guaranty incorporate lease terms requiring interpretation or extrinsic evidence?

Are there material disputes regarding calculation methods, security deposit application, or acceleration formulas?

If the guaranty requires evidence beyond the document itself, CPLR 3213 is improper. Defeating this motion converts the case to standard litigation, buying 12–18 months of negotiation time and significantly increasing settlement leverage.

Asset Protection & Exemption Planning

My LL.M. in Taxation and expertise in New York exemption law allows me to map realistic exposure before enforcement begins.

Protected assets and income include:

Retirement accounts: CPLR 5205(c) provides conclusive presumption that ERISA-qualified plans and IRAs are spendthrift trusts exempt from creditor claims

Homestead exemption: CPLR 5206 protects up to $179,950 in home equity (NYC metropolitan area)

Income execution limits: CPLR 5231 caps garnishments at 10% of gross income, protecting 90% of wages

Exempt income streams: Social Security, disability payments, and certain pension income that creditors cannot reach

Tenancy by entirety: Real property owned jointly with a spouse may be protected from individual creditor claims

Pre-Judgment Structuring Considerations:

Single-purpose LLCs are designed to fail when the business cannot pay rent—that's their function. The key is ensuring personal assets are protected before default occurs. Post-default transfers trigger fraudulent conveyance analysis under Debtor and Creditor Law Article 10, potentially voiding the protection.

We advise on irrevocable trust planning (distinguishing protective irrevocable structures from revocable trusts that offer no creditor protection), income stream management (restructuring compensation to clarify what landlords can reach through income executions), and exemption planning that maximizes statutory protections available under New York law.

Post-Judgment Enforcement Defense

If a guarantor arrives after judgment is entered, we provide enforcement defense services including vacating default judgments under CPLR 5015 based on lack of service or excusable default, fighting bank restraints by filing exemption claim forms under CPLR 5222-a to release frozen accounts containing exempt funds, and limiting garnishments that exceed statutory caps or impinge on reasonable living expenses.

When Strategic Advisory Makes Sense

Strategic consultation is most valuable at three stages:

- Before signing: Reviewing proposed guaranty language to understand scope, identify negotiable limitations, assess worst-case exposure, and determine if modifications can limit liability to specific time periods or cap maximum exposure.

- Before default: Planning exit strategies when business struggles become apparent, documenting compliance with surrender provisions, protecting assets before enforcement begins, and analyzing cross-default implications across multiple lease portfolios.

- After demand: Analyzing landlord claims for procedural defects, contractual non-compliance, notice failures, mitigation duty violations, and damage calculation errors before responding to demand letters or lawsuits.

Early engagement preserves options. Once landlords obtain judgments and begin enforcement through bank restraints and wage garnishments, the procedural landscape narrows significantly and asset protection becomes more difficult.

The Defense Advantage

Most commercial lease attorneys focus on deal-making. I focus on enforcement mechanics. Understanding how landlords collect—and which legal protections limit their reach—allows me to identify vulnerabilities in their claims and protections for your assets that transaction counsel may not recognize.