This blog series focuses on tax audits of attorneys. Why? Because I'm an attorney, and am highly interested in how attorneys wind up in hot water with the IRS. Even though this series focuses on attorneys, the below demands could apply to any taxpayer conducting a trade or business.

This particular post contains a sample of an Information Document Request (IDR), and a sample of a Bank Document Request. These should give you a feel for the intensity of an IRS audit, if you’re a lucky target. Each taxpayer has unique tax circumstances. Each industry has unique taxation rules and circumstances. I personally enjoy studying industry behavior from the IRS' perspective.

Three points to remember when considering your responses:

- Provide a timely, thorough response. If you need more time, request an extension early.

- Prepare to substantiate all transactions, and explain the transactions in question.

- Present your facts and tax-return position in a coherent and organized way.

Information Document Request (IDR)

- All books and records: Cash receipts and disbursements journals, appointment book(s), client's card index, daily log or receipts book, journals of receipts and disbursements from trust funds, payroll journals, subsidiary ledgers, and chart of accounts

- Bank statements, cancelled checks, and deposit slips for all personal, business and trust accounts for the periods 1/__ through 1/__

- Bank reconciliation statements for the last month of the calendar year for all business and trust accounts.

- Investment records, account statements and other investment information

- Work papers used to prepare/reconcile books with the tax return

- Client list for the year(s) under examination.

- Copies of Forms 1040 for 20__ and 20__ .

- Copies of Forms 8300 filed for the examination year.

- Employers quarterly tax returns--Federal and State (Forms 940, 941, and State Forms) for the year under examination to the present.

- Employee(s) Forms W-2 and W-4 for the year under examination and all Forms 1099 received and issued.

- Invoices covering all acquisitions and dispositions of capital assets during the examination year and verification of basis for the assets shown on the depreciation schedule.

- Records substantiating the claimed travel & entertainment expenses as required by IRC § 274--diary, itinerary, invoices, cancelled checks, names, dates, business purpose, etc.

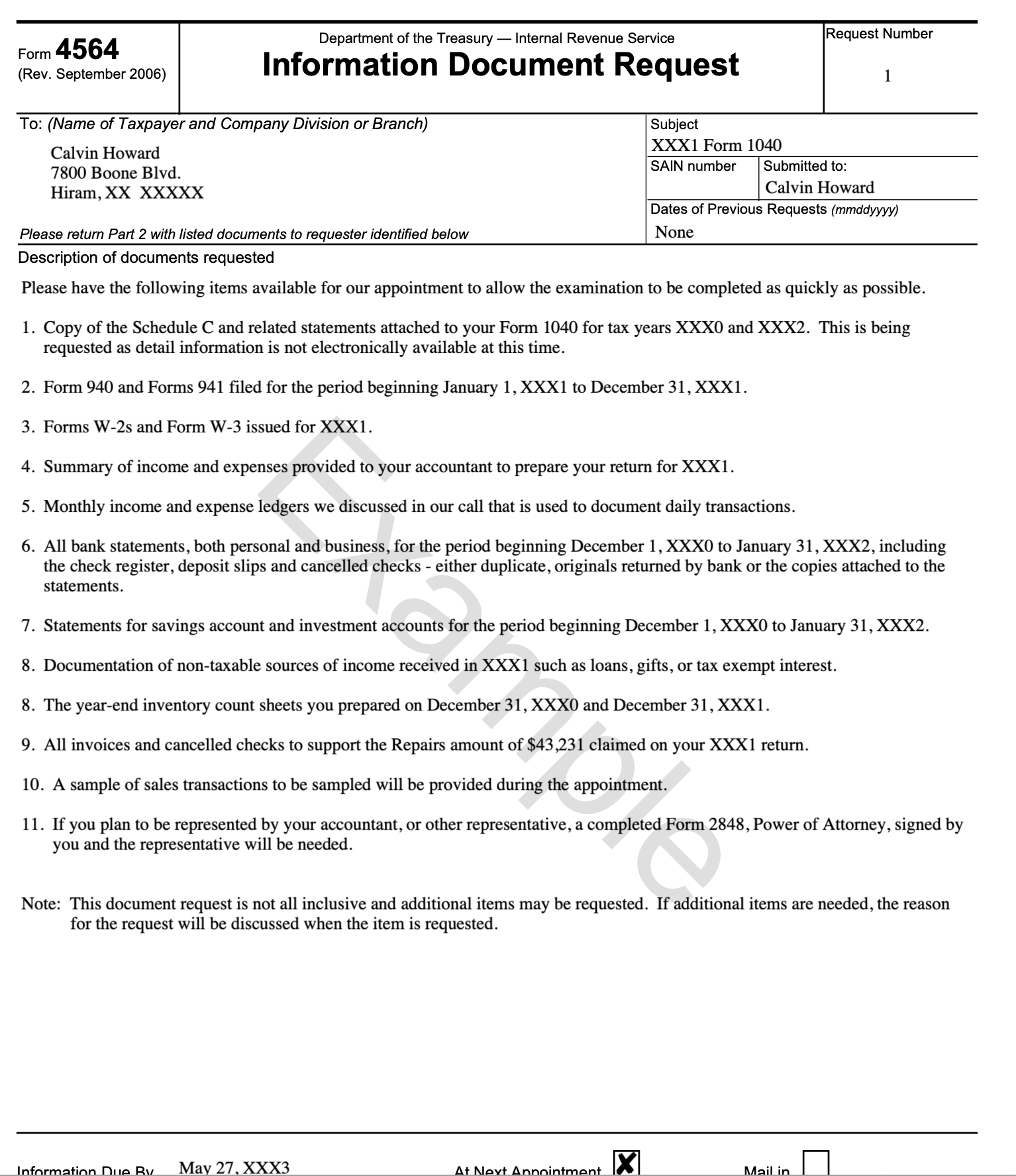

An IDR is issued on Form 4564, a sample of which is pasted below. These requests are taken directly from the IRS’ Attorneys Audit Technique Guide.

Bank Document Request List

1. The following information regarding all open or closed checking (interest and non-interest bearing) and savings accounts:

- Signature cards

- Bank statements

- Cancelled checks - front & back

- Deposit tickets & items

- Credit and debit memos

- Wire transfer records g. Forms 1099 or back-up withholding statements.

2. Retained copies of all open or closed bank loan or mortgage documents:

- Loan application

- Loan ledger sheet

- Copy of loan disbursement document

- Copy of loan repayment document

- Loan correspondence file

- Collateral agreements

- Copies of notes or other instruments reflecting the obligation to pay

- Copies of real estate mortgages, chattel mortgages, or other security for bank loans

- Copies of annual interest paid statements

- Copies of loan amortization statements

- Copies of any and all documents in loan package records.

3. Certificates of deposit (purchased or redeemed):

- Copies of the certificates

- Records pertaining to interest earned, withdrawn or reinvested

- Forms 1099 or back-up withholding statements.

4. Open or closed investment or security custodian accounts:

- Documents reflecting purchase of security

- Documents reflecting negotiation of security

- Safekeeping records and logs

- Receipts for the delivery of securities

- Copies of annual interest paid statements.

5. All open or closed IRA, Keogh, and other retirement plans:

- Account statements

- Investment, transfer, and redemption confirmation slips

- Documents reflecting purchase of investment

- Documents reflecting redemption of investment

- Copies of annual interest earned statements.

6. Customer correspondence file.

7. Retained copies of all Cashier's, Manager's, Bank, or Traveler's checks and money orders.

8. Wire transfer files:

- Fed wire, Swift, or other documents reflecting transfer of funds to, from, or on behalf of (the subject's name)

- Documents reflecting source of funds for wire out c. Documents reflecting disposition of wire transfer in.

9. Retained copies of all open or closed safe deposit box rental and entry records.

10. Open or closed credit card files

a. Applications for credit cards

- Monthly statements

- Copies of charges

- Copies of documents used to make payments on account.

11. Retained copies of Currency Transaction Reports

12. Retained copies of bank's CTR Exempt List (if subject is exempt) and documents reflecting justification for exemption.

A Potential Follow-up Summons

If the IRS is unsatisfied with your responses, the Revenue Agent assigned to your case may issue a summons. To wield a summons, the IRS must satisfy the four conditions set forth in a Supreme Court case, United States v. Powell:

- The inquiry is being conducted for a legitimate purpose

- The inquiry is relevant to the purpose

- The information being requested is not already within the possession of the IRS; and

- The administrative steps that the Internal Revenue Code requires have been taken.

Only the District Court can penalize taxpayers for failing to comply with the summons.

If matters do escalate, and you are served with a summons, a tax lawyer would spend good time thinking about the following rights and privileges:

- The right to be represented by counsel

- The right to invoke the 5th amendment purpose against self-incrimination

- The right to assert various other privileges including the spousal and marital privileges, the doctor-patient privilege, or the federally authorized tax practitioner privilege; and

- The right to make an audio recording of the summons hearing

Please see my prior blogs on expense issues and income issues for attorneys.

Feel free to call or write me if you’ve received a Notice or Letter from the IRS seeking information.

Although tax advisors and lawyers are generally not allowed to render tax advice based on the chances of an audit, you’ll likely enjoy this Youtube Video outlining the respective chances of getting audited based on income levels. Low income levels are general indicators of a lower audit rates, but other activities or transactions are believed to increase your audit levels. They are:

- Filing a Schedule C, including losses on a Schedule C, capital losses, and casualty losses

- Size of losses

- High deductions compared to income (i.e. charitable contributions)

- Not reporting all income (discussed in prior blog entry)

For your viewing pleasure, I paste below a sample, completed Information Document Request.